by

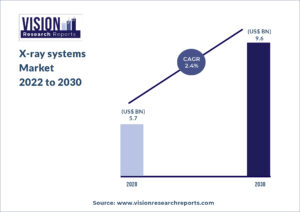

by The global X-ray systems market size was valued at USD 5.7 billion in 2020, and is predicted to be worth around USD 9.6 billion by 2030, registering a CAGR of 2.4% during the forecast period 2022 to 2030.

Download Exclusive Sample of Report@ https://www.visionresearchreports.com/report/sample/39115

Table of Contents

X-ray systems Market Growth Factors

Technological advancements in the healthcare sector and supportive investments by the government are driving the market. In addition, increase in the demand for early-stage diagnosis of chronic diseases and screening programs are expected to boost market growth.

Emerging innovations in the x-ray systems is expanding the market size, such as integration of Artificial Intelligence (AI) in medical imaging systems, robotic, and mobile x-ray systems have made the technology more accessible for use in limited-resource communities around the world. For instance, in March 2021, Philips healthcare announced partnership with Lunit, a leading medical AI startup, with this collaboration Lunit’s INSIGHT CXR chest detection suite will be incorporated into Philips diagnostic x-ray suite, to achieve better patient outcomes, improve the experience of patients and staff, and lower the cost of care.

The COVID-19 pandemic has posed challenges and changed healthcare systems globally. Radiology has considerably improved patient care in this crisis, owing to rapid advancements.The first imaging procedure that played an important role in the treatment of COVID-19 was chest radiography, since it plays a major role in the diagnosis of COVID-19.

X-ray systems Market Report Coverage

| Report Scope | Details |

| Market Size | US$ 9.6 billion by 2030 |

| Growth Rate | CAGR of 2.4% From 2022 to 2030 |

| Largest Market | North America |

| Base Year | 2021 |

| Forecast Period | 2022 to 2030 |

| Segments Covered | Modality, Technology, Mobility, End use |

| Regional Scope | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Companies Mentioned | Koninklijke Philips N.V.; Siemens Healthineers AG; GE Healthcare; Canon Medical Systems; Shimadzu Corporation; FUJIFILM SonoSite, Inc.; Carestream; Mindray Medical International Limited; Hologic, Inc.; New Medical Imaging; AGFA |

By Modality Analysis

The radiography segment dominated the market and accounted for the largest revenue share of more than 49.0% in 2021. The segment is further expected to continue its dominance over the forecast period.

As this system has a wide range of applications and is less expensive and time-consuming than other systems. Furthermore, the increasing technological advancements is expected to boost market growth for this segment.

The mammography segment is also expected to grow at a significant rate over the forecast period, owing to the increasing incidence of breast cancer and rising awareness about the same amongst the population.

By Technology Analysis

The Computed Radiography (CR) segment dominated the market for x-ray systems and accounted for the largest revenue share of 54.6% in 2021, owing to its lower initial costs.

CR is the first digital replacement for traditional x-ray film radiography with cassette-based Phosphor Storage Plates (PSP), which provides significant benefits such as the elimination of consumables and a significant reduction in image development time.

The Digital Radiography (DR) segment is anticipated to witness the fastest growth rate over the forecast period. There is a growing demand for DR since this system produces, high contrast resolution images at lower ionizing radiation using flat panel detectors (FPD).

By Mobility Analysis

The stationary x-ray systems segment dominated the market and held the largest revenue share of 65.0%in 2021. In developing countries, where the adoption of new technology is slower, stationary x-ray systems have been found to be in high demand.

An increase in demand for mobile x-ray systems is noted, ever since the covid-19 pandemic as this system has the flexibility to be carried around the hospital or to a patient’s home, thus decreasing the risk of virus transmission.

By End-use Analysis

The hospital segment dominated the market and accounted for the largest revenue share of 68.7% in 2021. In outpatient settings, x-ray system is a substantial source of revenue, also there is an increase in the number of patients visiting hospitals with various chronic disorders.

Siemens Healthineers announced its partnership with Kantonsspital Baden, a hospital in Switzerland, this partnership involves imaging system procurement and maintenance, training programs, and research support.

The diagnostic imaging center segment is expected to witness significant growth during the forecast period. Imaging centers provide a comprehensive range of diagnostic and preventative health services.

The growing patient population with chronic disorders is an opportunity for radiologists to provide stand-alone outpatient imaging centers.

By Regional Analysis

North America dominated the market and accounted for the largest revenue share of 30% in 2021. The market is being influenced by factors such as increasing adoption of modern technology and improved healthcare infrastructure, strong purchasing power, and a fair reimbursement framework.

In Asia Pacific, the market for x-ray systems is estimated to witness the fastest CAGR during the forecast period owing to the increased demand for better imaging devices and supportive government initiatives for improving healthcare infrastructure in the region.

Read also @ Cardiac Resynchronization Therapy Market to Reach US$ 10.8 Bn by 2030

Major Key Players Covered in The X-ray systems Market Report include

- Koninklijke Philips N.V.

- Siemens Healthineers AG

- GE Healthcare

- Canon Medical Systems

- Shimadzu Corporation

- FUJIFILM SonoSite, Inc.

- Carestream

- Mindray Medical International Limited

- Hologic, Inc

- New Medical Imaging

- AGFA

X-ray systems Market Segmentation

- By Modality

- Radiography

- Fluoroscopy

- Mammography

- By Technology

- Digital radiography

- Computed radiography

- By Mobility

- Stationary

- Mobile

- By End-use

- Hospitals

- Diagnostic imaging centres

- Regional

- North America

- U.S.

- Canada

- Europe

- U.K.

- Germany

- France

- Italy

- Spain

- Asia Pacific

- Japan

- China

- India

- Australia

- South Korea

- Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Middle East and Africa

- South Africa

- Saudi Arabia

- UAE

- North America

Table of Contents

Chapter 1. Introduction

1.1. Research Objective

1.2. Scope of the Study

1.3. Definition

Chapter 2. Research Methodology

2.1. Research Approach

2.2. Data Sources

2.3. Assumptions & Limitations

Chapter 3. Executive Summary

3.1. Market Snapshot

Chapter 4. X-ray systems Market Variables and Scope

4.1. Introduction

4.2. Market Classification and Scope

4.3. Industry Value Chain Analysis

4.3.1. Raw Material Procurement Analysis

4.3.2. Sales and Mobility Analysis

4.3.3. Downstream Buyer Analysis

Chapter 5. X-ray systems Market Dynamics Analysis and Trends

5.1. Market Dynamics

5.1.1. Market Drivers

5.1.2. Market Restraints

5.1.3. Market Opportunities

5.2. Porter’s Five Forces Analysis

5.2.1. Bargaining power of suppliers

5.2.2. Bargaining power of buyers

5.2.3. Threat of substitute

5.2.4. Threat of new entrants

5.2.5. Degree of competition

Chapter 6. Competitive Landscape

6.1.1. Company Market Share/Positioning Analysis

6.1.2. Key Strategies Adopted by Players

6.1.3. Vendor Landscape

6.1.3.1. List of Suppliers

6.1.3.2. List of Buyers

Chapter 7. Global X-ray Systems Market, By Modality

7.1. X-ray Systems Market, by Modality, 2021-2030

7.1.1. Radiography

7.1.1.1. Market Revenue and Forecast (2019-2030)

7.1.2. Fluoroscopy

7.1.2.1. Market Revenue and Forecast (2019-2030)

7.1.3. Mammography

7.1.3.1. Market Revenue and Forecast (2019-2030)

Chapter 8. Global X-ray Systems Market, By Technology

8.1. X-ray Systems Market, by Technology, 2021-2030

8.1.1. Digital Radiography

8.1.1.1. Market Revenue and Forecast (2019-2030)

8.1.2. Computed Radiography

8.1.2.1. Market Revenue and Forecast (2019-2030)

Chapter 9. Global X-ray Systems Market, By Mobility

9.1. X-ray Systems Market, by Mobility, 2021-2030

9.1.1. Stationary

9.1.1.1. Market Revenue and Forecast (2019-2030)

9.1.2. Mobile

9.1.2.1. Market Revenue and Forecast (2019-2030)

Chapter 10. Global X-ray Systems Market, By End-use

10.1. X-ray Systems Market, by End-use, 2021-2030

10.1.1. Hospitals

10.1.1.1. Market Revenue and Forecast (2019-2030)

10.1.2. Diagnostic imaging centres

10.1.2.1. Market Revenue and Forecast (2019-2030)

Chapter 11. Global X-ray Systems Market, Regional Estimates and Trend Forecast

11.1. North America

11.1.1. Market Revenue and Forecast, by Modality (2019-2030)

11.1.2. Market Revenue and Forecast, by Technology (2019-2030)

11.1.3. Market Revenue and Forecast, by Mobility (2019-2030)

11.1.4. Market Revenue and Forecast, by End-use (2019-2030)

11.1.5. U.S.

11.1.5.1. Market Revenue and Forecast, by Modality (2019-2030)

11.1.5.2. Market Revenue and Forecast, by Technology (2019-2030)

11.1.5.3. Market Revenue and Forecast, by Mobility (2019-2030)

11.1.5.4. Market Revenue and Forecast, by End-use (2019-2030)

11.1.6. Rest of North America

11.1.6.1. Market Revenue and Forecast, by Modality (2019-2030)

11.1.6.2. Market Revenue and Forecast, by Technology (2019-2030)

11.1.6.3. Market Revenue and Forecast, by Mobility (2019-2030)

11.1.6.4. Market Revenue and Forecast, by End-use (2019-2030)

11.2. Europe

11.2.1. Market Revenue and Forecast, by Modality (2019-2030)

11.2.2. Market Revenue and Forecast, by Technology (2019-2030)

11.2.3. Market Revenue and Forecast, by Mobility (2019-2030)

11.2.4. Market Revenue and Forecast, by End-use (2019-2030)

11.2.5. UK

11.2.5.1. Market Revenue and Forecast, by Modality (2019-2030)

11.2.5.2. Market Revenue and Forecast, by Technology (2019-2030)

11.2.5.3. Market Revenue and Forecast, by Mobility (2019-2030)

11.2.5.4. Market Revenue and Forecast, by End-use (2019-2030)

11.2.6. Germany

11.2.6.1. Market Revenue and Forecast, by Modality (2019-2030)

11.2.6.2. Market Revenue and Forecast, by Technology (2019-2030)

11.2.6.3. Market Revenue and Forecast, by Mobility (2019-2030)

11.2.6.4. Market Revenue and Forecast, by End-use (2019-2030)

11.2.7. France

11.2.7.1. Market Revenue and Forecast, by Modality (2019-2030)

11.2.7.2. Market Revenue and Forecast, by Technology (2019-2030)

11.2.7.3. Market Revenue and Forecast, by Mobility (2019-2030)

11.2.7.4. Market Revenue and Forecast, by End-use (2019-2030)

11.2.8. Rest of Europe

11.2.8.1. Market Revenue and Forecast, by Modality (2019-2030)

11.2.8.2. Market Revenue and Forecast, by Technology (2019-2030)

11.2.8.3. Market Revenue and Forecast, by Mobility (2019-2030)

11.2.8.4. Market Revenue and Forecast, by End-use (2019-2030)

11.3. APAC

11.3.1. Market Revenue and Forecast, by Modality (2019-2030)

11.3.2. Market Revenue and Forecast, by Technology (2019-2030)

11.3.3. Market Revenue and Forecast, by Mobility (2019-2030)

11.3.4. Market Revenue and Forecast, by End-use (2019-2030)

11.3.5. India

11.3.5.1. Market Revenue and Forecast, by Modality (2019-2030)

11.3.5.2. Market Revenue and Forecast, by Technology (2019-2030)

11.3.5.3. Market Revenue and Forecast, by Mobility (2019-2030)

11.3.5.4. Market Revenue and Forecast, by End-use (2019-2030)

11.3.6. China

11.3.6.1. Market Revenue and Forecast, by Modality (2019-2030)

11.3.6.2. Market Revenue and Forecast, by Technology (2019-2030)

11.3.6.3. Market Revenue and Forecast, by Mobility (2019-2030)

11.3.6.4. Market Revenue and Forecast, by End-use (2019-2030)

11.3.7. Japan

11.3.7.1. Market Revenue and Forecast, by Modality (2019-2030)

11.3.7.2. Market Revenue and Forecast, by Technology (2019-2030)

11.3.7.3. Market Revenue and Forecast, by Mobility (2019-2030)

11.3.7.4. Market Revenue and Forecast, by End-use (2019-2030)

11.3.8. Rest of APAC

11.3.8.1. Market Revenue and Forecast, by Modality (2019-2030)

11.3.8.2. Market Revenue and Forecast, by Technology (2019-2030)

11.3.8.3. Market Revenue and Forecast, by Mobility (2019-2030)

11.3.8.4. Market Revenue and Forecast, by End-use (2019-2030)

11.4. MEA

11.4.1. Market Revenue and Forecast, by Modality (2019-2030)

11.4.2. Market Revenue and Forecast, by Technology (2019-2030)

11.4.3. Market Revenue and Forecast, by Mobility (2019-2030)

11.4.4. Market Revenue and Forecast, by End-use (2019-2030)

11.4.5. GCC

11.4.5.1. Market Revenue and Forecast, by Modality (2019-2030)

11.4.5.2. Market Revenue and Forecast, by Technology (2019-2030)

11.4.5.3. Market Revenue and Forecast, by Mobility (2019-2030)

11.4.5.4. Market Revenue and Forecast, by End-use (2019-2030)

11.4.6. North Africa

11.4.6.1. Market Revenue and Forecast, by Modality (2019-2030)

11.4.6.2. Market Revenue and Forecast, by Technology (2019-2030)

11.4.6.3. Market Revenue and Forecast, by Mobility (2019-2030)

11.4.6.4. Market Revenue and Forecast, by End-use (2019-2030)

11.4.7. South Africa

11.4.7.1. Market Revenue and Forecast, by Modality (2019-2030)

11.4.7.2. Market Revenue and Forecast, by Technology (2019-2030)

11.4.7.3. Market Revenue and Forecast, by Mobility (2019-2030)

11.4.7.4. Market Revenue and Forecast, by End-use (2019-2030)

11.4.8. Rest of MEA

11.4.8.1. Market Revenue and Forecast, by Modality (2019-2030)

11.4.8.2. Market Revenue and Forecast, by Technology (2019-2030)

11.4.8.3. Market Revenue and Forecast, by Mobility (2019-2030)

11.4.8.4. Market Revenue and Forecast, by End-use (2019-2030)

11.5. Latin America

11.5.1. Market Revenue and Forecast, by Modality (2019-2030)

11.5.2. Market Revenue and Forecast, by Technology (2019-2030)

11.5.3. Market Revenue and Forecast, by Mobility (2019-2030)

11.5.4. Market Revenue and Forecast, by End-use (2019-2030)

11.5.5. Brazil

11.5.5.1. Market Revenue and Forecast, by Modality (2019-2030)

11.5.5.2. Market Revenue and Forecast, by Technology (2019-2030)

11.5.5.3. Market Revenue and Forecast, by Mobility (2019-2030)

11.5.5.4. Market Revenue and Forecast, by End-use (2019-2030)

11.5.6. Rest of LATAM

11.5.6.1. Market Revenue and Forecast, by Modality (2019-2030)

11.5.6.2. Market Revenue and Forecast, by Technology (2019-2030)

11.5.6.3. Market Revenue and Forecast, by Mobility (2019-2030)

11.5.6.4. Market Revenue and Forecast, by End-use (2019-2030)

Chapter 12. Company Profiles

12.1. Koninklijke Philips N.V.

12.1.1. Company Overview

12.1.2. Modality Offerings

12.1.3. Financial Performance

12.1.4. Recent Initiatives

12.2. Siemens Healthineers AG

12.2.1. Company Overview

12.2.2. Modality Offerings

12.2.3. Financial Performance

12.2.4. Recent Initiatives

12.3. GE Healthcare

12.3.1. Company Overview

12.3.2. Modality Offerings

12.3.3. Financial Performance

12.3.4. Recent Initiatives

12.4. Canon Medical Systems

12.4.1. Company Overview

12.4.2. Modality Offerings

12.4.3. Financial Performance

12.4.4. Recent Initiatives

12.5. Shimadzu Corporation

12.5.1. Company Overview

12.5.2. Modality Offerings

12.5.3. Financial Performance

12.5.4. Recent Initiatives

12.6. FUJIFILM SonoSite, Inc.

12.6.1. Company Overview

12.6.2. Modality Offerings

12.6.3. Financial Performance

12.6.4. Recent Initiatives

12.7. Carestream

12.7.1. Company Overview

12.7.2. Modality Offerings

12.7.3. Financial Performance

12.7.4. Recent Initiatives

12.8. Mindray Medical International Limited

12.8.1. Company Overview

12.8.2. Modality Offerings

12.8.3. Financial Performance

12.8.4. Recent Initiatives

12.9. Hologic, Inc

12.9.1. Company Overview

12.9.2. Modality Offerings

12.9.3. Financial Performance

12.9.4. Recent Initiatives

12.10. New Medical Imaging

12.10.1. Company Overview

12.10.2. Modality Offerings

12.10.3. Financial Performance

12.10.4. Recent Initiatives

Chapter 13. Research Methodology

13.1. Primary Research

13.2. Secondary Research

13.3. Assumptions

Chapter 14. Appendix

14.1. About Us

14.2. Glossary of Terms

Buy this Research Report study@ https://www.visionresearchreports.com/report/cart/39115

Contact Us:

Vision Research Reports

Call: +1 9197 992 333