by

by

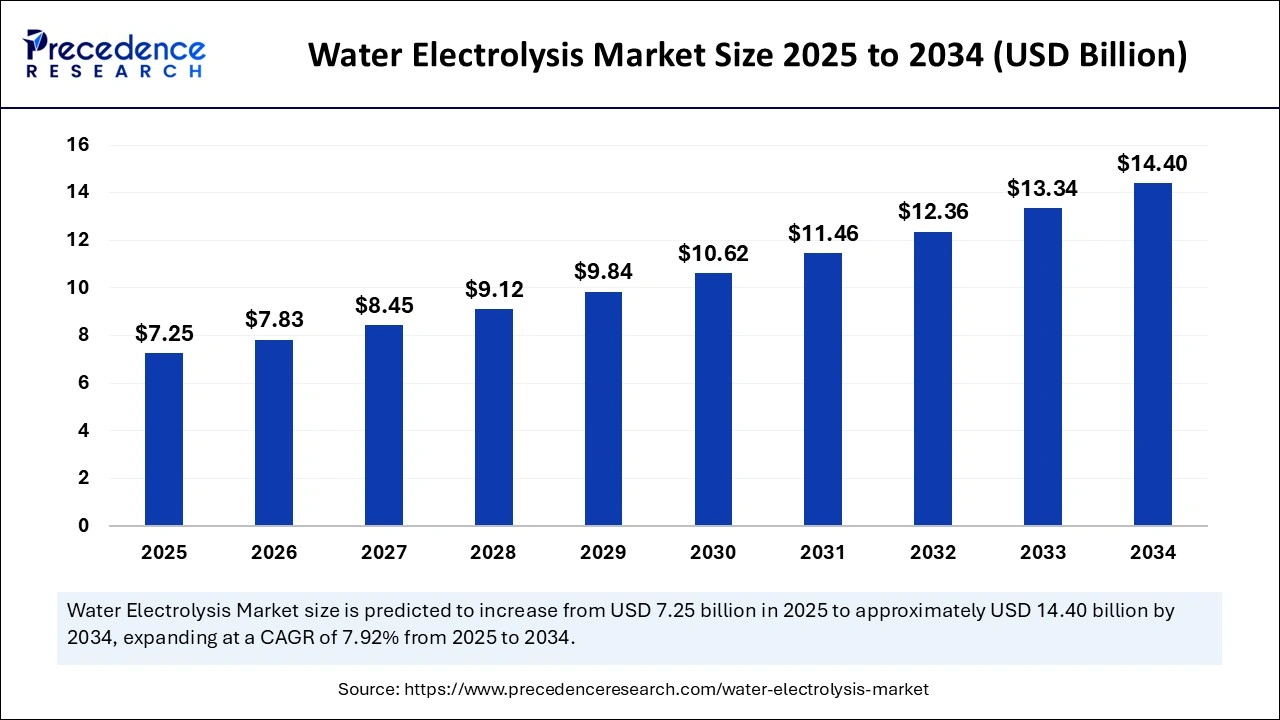

Water Electrolysis Market Key Points

- Asia Pacific led the global market in 2024, accounting for over 43% of the total revenue share.

- North America is projected to register the fastest CAGR throughout the forecast period.

- By product, the alkaline water electrolysis segment dominated the market with a 59% revenue share in 2024.

- The proton exchange membrane segment is expected to grow at the highest CAGR between 2025 and 2034.

- Based on end-use, the chemicals segment held the largest revenue share of 43% in 2024.

- The power plants segment is anticipated to expand at the fastest growth rate over the forecast years.

Water Electrolysis Market Overview

The water electrolysis market is experiencing rapid growth as global economies transition toward cleaner energy systems and decarbonization strategies. Water electrolysis is a process that splits water into hydrogen and oxygen using electricity, producing high-purity hydrogen gas. When powered by renewable energy sources such as solar or wind, this process is known as “green hydrogen” production—a vital component in achieving net-zero emission targets. Unlike conventional hydrogen production methods (e.g., steam methane reforming), water electrolysis emits no carbon dioxide, positioning it as a cornerstone of the emerging hydrogen economy.

The market is gaining momentum across industries including energy, transportation, chemical manufacturing, and steel production, where green hydrogen serves as a fuel, feedstock, or reducing agent. With increasing governmental support, climate policies, and private investments, water electrolysis is moving from pilot projects to commercial-scale deployments. The market comprises several technologies—primarily alkaline electrolysis (AEL), proton exchange membrane (PEM) electrolysis, and solid oxide electrolysis cells (SOEC)—each suited to different operational environments and output scales. As the demand for clean hydrogen escalates, water electrolysis is poised to become a central pillar of sustainable industrial infrastructure.

Water Electrolysis Market Growth Factors

A key factor driving market growth is the global push toward decarbonization. Governments and corporations alike are committing to aggressive carbon reduction goals, and green hydrogen production through electrolysis is a critical pathway to achieving these ambitions. Hydrogen can decarbonize sectors that are otherwise difficult to electrify, such as heavy industry, shipping, and aviation.

Another growth accelerator is the declining cost of renewable energy, particularly solar and wind, which enhances the economic viability of water electrolysis. As electricity accounts for a significant portion of electrolysis costs, cheaper renewables directly improve the competitiveness of green hydrogen.

Technological advancements in electrolyzer design, materials, and efficiency are also contributing to market expansion. Innovations in membrane technology, catalysts, and stack configurations are making electrolyzers more durable, scalable, and affordable. Simultaneously, larger-scale electrolysis plants are coming online, supported by modular designs and standardized production approaches.

Additionally, increasing public and private investment is fueling growth. Multi-billion-dollar hydrogen strategies by the EU, U.S., Japan, and others, alongside support from companies like Siemens Energy, ITM Power, and Nel Hydrogen, are building robust ecosystems for electrolysis deployment.

Impact of AI on the Water Electrolysis Market

Artificial Intelligence (AI) is beginning to play a transformative role in the water electrolysis market by optimizing operations, improving efficiency, and enabling predictive analytics. In production environments, AI algorithms monitor and control electrolyzer performance in real time, adjusting parameters such as voltage, current density, and water flow to maximize hydrogen yield and reduce energy consumption.

AI also enhances predictive maintenance, identifying anomalies in temperature, pressure, or gas purity that may indicate wear or failure. This minimizes downtime and maintenance costs, which are crucial for the economic scalability of electrolysis systems. Moreover, AI-driven models can simulate electrolyzer performance under varying renewable power inputs, helping operators balance load variability and improve grid integration.

In addition, AI supports supply chain optimization and system design. Machine learning is used to model the entire hydrogen production ecosystem—from water sourcing and purification to storage and transport—enabling the design of more efficient, integrated systems. It can also forecast hydrogen demand based on market trends and usage data, allowing producers to align output with consumption patterns.

Furthermore, AI is instrumental in accelerating materials discovery. By analyzing vast datasets on catalysts, electrodes, and membranes, AI can identify optimal materials for future electrolyzer generations, reducing R&D timelines and costs.

Market Drivers

Among the most powerful market drivers is the intensifying global focus on green energy and climate policy. The Paris Agreement, European Green Deal, U.S. Inflation Reduction Act, and similar frameworks have established hydrogen as a critical enabler of carbon neutrality, stimulating demand for water electrolysis.

The growing demand for clean hydrogen in industrial applications also drives market expansion. Green hydrogen is increasingly being used in ammonia and methanol production, petroleum refining, and as a feedstock for green steel. These applications require large-scale, low-carbon hydrogen sources—precisely what water electrolysis provides.

The proliferation of renewable energy capacity globally ensures a steady, cost-effective power source for electrolyzers. In regions with surplus renewable power, such as Australia, the Middle East, and North Africa, water electrolysis provides a means of storing and exporting clean energy in the form of hydrogen.

Additionally, government incentives and funding programs—including subsidies, tax credits, and research grants—are significantly lowering the barriers to market entry. These policies are encouraging both established players and startups to invest in electrolyzer technologies and infrastructure.

Opportunities

The water electrolysis market presents substantial opportunities for innovation and expansion. One of the biggest opportunities lies in scaling up electrolyzer capacity to gigawatt levels. Large-scale projects like the NEOM Green Hydrogen Project in Saudi Arabia or the HyDeal Ambition in Europe demonstrate the enormous potential for utility-scale hydrogen production.

Another promising area is the integration of water electrolysis with offshore wind farms and solar parks. Co-locating electrolyzers with renewable energy assets minimizes transmission losses and enables hydrogen production in remote, resource-rich areas for export via pipelines or liquefaction.

There is also significant potential in developing modular, decentralized electrolyzer units for use in microgrids, rural electrification, or fueling stations. These systems could enable hydrogen production at the point of use, supporting local industries, transportation fleets, and communities.

Further opportunities exist in cross-sector partnerships, where energy, technology, and industrial firms collaborate to build integrated hydrogen value chains. Joint ventures between electrolyzer manufacturers, utility providers, and logistics firms can create end-to-end ecosystems that accelerate hydrogen adoption.

Challenges

Despite its potential, the water electrolysis market faces several challenges. One of the main obstacles is the high capital cost of electrolyzer systems, especially for PEM and solid oxide technologies. Although costs are falling, they remain a barrier to widespread commercial adoption in price-sensitive regions.

Another challenge is the intermittent nature of renewable energy, which complicates consistent hydrogen production. Operating electrolyzers efficiently under variable power inputs requires sophisticated energy management and storage solutions, adding to system complexity.

Water availability and quality is a growing concern, especially in arid regions. Electrolysis requires purified water, and sourcing this sustainably—particularly in areas prone to drought—can limit project feasibility or increase operational costs.

Infrastructure limitations also hinder growth. The lack of hydrogen storage, distribution pipelines, and refueling stations slows downstream adoption and reduces the incentive to invest in upstream hydrogen production capacity.

Water Electrolysis Market Companies

- Asahi Kasei Corporation

- Cummins Inc.

- Hitachi Zosen Corporation

- ITM Power PLC

- Nel ASA

- Plug Power Inc.

- Siemens Energy AG

- Teledyne Energy Systems Inc. Ltd.

- ThyssenKrupp AG

- Toshiba Energy Systems & Solutions Corporation

Segments covered in the report

By Product Outlook

- Alkaline Water Electrolysis

- Proton Exchange Membrane

- Solid Oxide Electrolyte (SOE)

By End-use Outlook

- Chemicals

- Electronics & Semiconductor

- Others

- Petroleum

- Pharmaceuticals

- Power Plants

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East

- Africa

Read Also: Digital Legacy Market

Get this report to explore global market size, share, CAGR, and trends, featuring detailed segmental analysis and an insightful competitive landscape overview @ https://www.precedenceresearch.com/sample/6108

You can place an order or ask any questions, please feel free to contact at sales@precedenceresearch.com|+1 804 441 9344