by

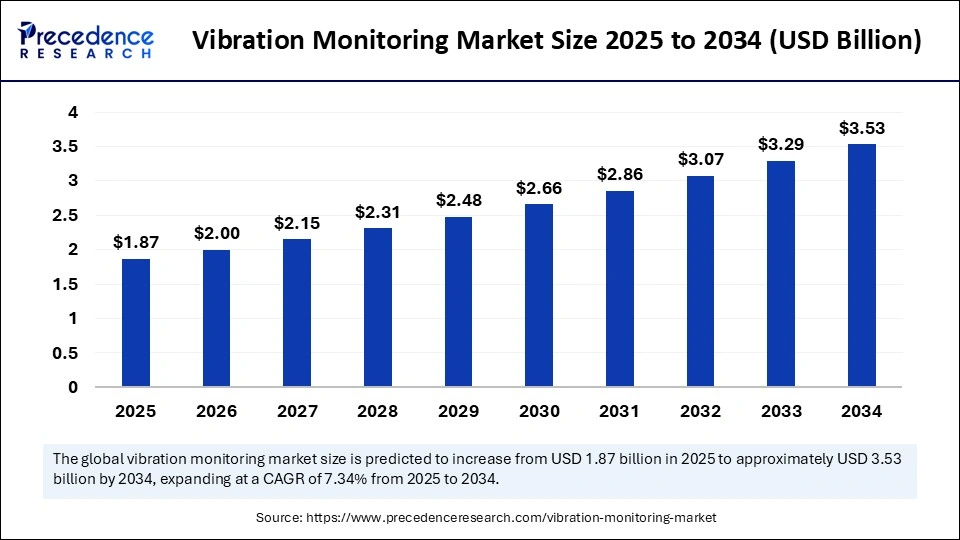

by The global vibration monitoring market size is estimated to gain around USD 3.53 billion by 2034 increasing from USD 1.74 billion in 2024, with a CAGR of 7.34%.

Vibration Monitoring Market Key Points

-

North America dominated the vibration monitoring market with the largest share in 2024.

-

Asia Pacific is projected to grow at the fastest CAGR during the forecast period.

-

By component, the hardware segment accounted for the largest market share in 2024.

-

The software segment, by component, is expected to grow at the fastest rate in the upcoming years.

-

By process, the portable vibration monitoring segment held the dominant share of the market in 2024.

-

The online vibration monitoring segment, by process, is projected to expand at the highest rate in the coming years.

-

By industry, the oil & gas segment led the market in 2024.

-

The automotive segment, by industry, is anticipated to grow at the fastest rate between 2025 and 2034.

Market Overview

The vibration monitoring market is a vital segment of the industrial automation and predictive maintenance ecosystem. It focuses on systems and solutions used to monitor mechanical vibrations in machinery and equipment to detect imbalances, misalignments, bearing failures, and other performance issues before they lead to costly breakdowns. These systems are extensively deployed across industries such as manufacturing, energy and power, oil and gas, aerospace, automotive, and mining. The market is gaining traction due to the increasing shift from reactive to preventive and predictive maintenance strategies. As companies aim to reduce unplanned downtimes, enhance equipment life, and improve operational efficiency, the adoption of vibration monitoring devices—ranging from portable sensors to fully integrated online systems—is accelerating. The integration of IoT and wireless technologies has further enhanced the reach and capability of vibration monitoring, enabling real-time data capture and remote diagnostics. As industrial automation expands globally, the vibration monitoring market is expected to witness strong and sustained growth over the coming years.

Growth Factors

Several key factors are contributing to the growth of the vibration monitoring market. Chief among them is the rising demand for predictive maintenance solutions. Industries are under pressure to minimize operational costs and improve asset reliability, and vibration monitoring plays a central role in enabling proactive maintenance decisions. Another significant growth driver is the advancement in sensor technologies, such as MEMS-based vibration sensors, which offer high accuracy, low power consumption, and cost efficiency.

Furthermore, the rise in equipment automation and smart factory initiatives—under frameworks such as Industry 4.0—is fueling the integration of advanced condition monitoring systems. These systems are no longer limited to critical assets but are being deployed across entire production lines. Additionally, growing concerns around worker safety and equipment health, especially in high-risk industries like oil and gas or power generation, are promoting the deployment of continuous vibration monitoring solutions to detect anomalies before they pose safety risks. Finally, the expansion of manufacturing hubs in emerging markets and the modernization of legacy industrial infrastructure worldwide are contributing to the market’s upward momentum.

Impact of AI on the Market

Artificial intelligence (AI) is revolutionizing the vibration monitoring landscape by enhancing fault detection, diagnosis, and decision-making capabilities. Traditional vibration analysis methods required significant manual interpretation by experienced analysts, but AI-powered systems can now analyze complex vibration data streams in real time to identify patterns, trends, and potential anomalies with greater accuracy and speed. Machine learning (ML) algorithms are trained on vast datasets to detect early signs of mechanical failures that may be invisible to the human eye or conventional threshold-based systems.

Moreover, AI enables predictive and prescriptive maintenance. Predictive algorithms forecast when a component is likely to fail, while prescriptive AI recommends the optimal maintenance action, reducing downtime and repair costs. AI also enhances the effectiveness of remote monitoring platforms, enabling operators to oversee machinery health across multiple sites from a central dashboard. In addition, natural language processing (NLP) can be integrated into analytics software to generate easy-to-understand diagnostic reports for operators and maintenance staff. As the volume of sensor data continues to grow, AI will become increasingly critical to extracting actionable insights and driving smarter maintenance practices in vibration monitoring.

Market Scope

| Report Coverage | Details |

| Market Size by 2034 | USD 3.53 Billion |

| Market Size in 2025 | USD 1.87 Billion |

| Market Size in 2024 | USD 1.74 Billion |

| Market Growth Rate from 2025 to 2034 | CAGR of 7.34% |

| Dominating Region | North America |

| Fastest Growing Region | Asia Pacific |

| Base Year | 2024 |

| Forecast Period | 2025 to 2034 |

| Segments Covered | Component, Process, Industry, and Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Market Drivers

The vibration monitoring market is driven by a convergence of industrial and technological trends. One of the primary drivers is the increasing need for equipment uptime and reliability, especially in process industries where any failure can lead to significant financial and safety risks. Another strong driver is the growing emphasis on condition-based maintenance strategies over traditional calendar-based maintenance, which often results in unnecessary servicing or overlooked issues.

Regulatory pressure in sectors such as oil and gas, mining, and transportation is also pushing organizations to adopt more sophisticated monitoring systems. Additionally, the widespread adoption of wireless and cloud-based monitoring systems allows for easier implementation in remote or difficult-to-access locations, significantly expanding the application landscape. The growth of smart manufacturing and digital twins is further increasing the demand for integrated vibration monitoring as part of comprehensive asset performance management (APM) strategies.

Opportunities

The market offers numerous opportunities for innovation and expansion. One of the most promising areas is the integration of vibration monitoring into IoT ecosystems, allowing real-time asset tracking and seamless data sharing across platforms. This paves the way for end-to-end condition monitoring that combines vibration data with temperature, acoustic, and lubrication analysis to provide a complete health picture of assets.

There is also a growing opportunity in the development of low-cost, plug-and-play wireless vibration sensors for small- and medium-sized enterprises (SMEs), many of which lack the resources to invest in large-scale industrial automation but still seek reliable maintenance solutions. Edge computing, where vibration data is analyzed at the source rather than being transmitted to the cloud, is another innovation poised to enhance system responsiveness and reduce latency.

Additionally, the emerging demand for vibration monitoring in renewable energy assets, such as wind turbines and hydroelectric plants, opens new market segments as the global energy mix shifts. Finally, the expansion of infrastructure projects and industrial growth in developing regions presents lucrative opportunities for both vendors and service providers specializing in vibration diagnostics and condition monitoring.

Challenges

Despite its many advantages, the vibration monitoring market faces certain challenges. High initial setup costs and integration complexities often deter adoption, particularly among smaller companies or industries with constrained budgets. Additionally, lack of skilled personnel to interpret vibration data and use monitoring systems effectively remains a persistent issue in many regions.

Another major challenge is the standardization of data formats and interoperability across different hardware and software platforms. Many industries use equipment from multiple manufacturers, and achieving seamless integration between vibration monitoring systems and legacy machines or enterprise systems like SCADA or ERP is not always straightforward. Data security and privacy concerns also loom large, particularly with cloud-connected and AI-driven systems handling sensitive operational data.

Moreover, while AI offers significant advantages, model training and accuracy can be hindered by limited historical failure data in certain industries, making it difficult to build reliable predictive systems. Addressing these challenges requires industry-wide collaboration, investment in training, and ongoing R&D to create more accessible, interoperable, and user-friendly solutions.

Regional Outlook

The North American market leads in terms of adoption, driven by advanced manufacturing, strong industrial automation infrastructure, and the presence of major players in the U.S. and Canada. The region’s focus on operational excellence, combined with regulatory standards in industries such as oil and gas and aerospace, supports sustained demand for vibration monitoring solutions.

Europe follows closely, particularly in countries like Germany, the UK, and France, where Industry 4.0 initiatives are well underway. The European market also benefits from a strong emphasis on environmental sustainability and machinery safety, further encouraging adoption.

The Asia Pacific region is poised for the fastest growth due to rapid industrialization, the expansion of manufacturing sectors, and rising awareness of asset reliability in countries like China, India, Japan, and South Korea. Increasing investment in smart factories and government support for digital transformation in industries are fueling the demand for vibration monitoring in the region.

Latin America, the Middle East, and Africa represent emerging markets, where modernization of industrial infrastructure and resource-based industries such as mining and oil & gas are key drivers. However, these regions also face challenges related to funding, training, and infrastructure, which may slow down adoption compared to more developed markets.

Vibration Monitoring Market Companies

- Honeywell International Inc

- Emerson Electric Co.

- SKF

- Schaeffler AG

- Analog Device Inc.

- ALS

- Teledyne FLIR LLC

- Parker Hannifin Corp

- Rockwell Automation

- Baker Hughes Company

Segments Covered in the Report

By Component

- Hardware

- Software

- Services

By Process

- Online Vibration Monitoring

- Portable Vibration Monitoring

By Industry

- Oil & Gas

- Power Generation

- Mining & Metals

- Chemicals

- Automotive

- Aerospace

- Food & Beverages

- Other

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Read Also: Special Mission Aircraft Market

Get this report to explore global market size, share, CAGR, and trends, featuring detailed segmental analysis and an insightful competitive landscape overview @ https://www.precedenceresearch.com/sample/6125

You can place an order or ask any questions, please feel free to contact at sales@precedenceresearch.com|+1 804 441 9344