by

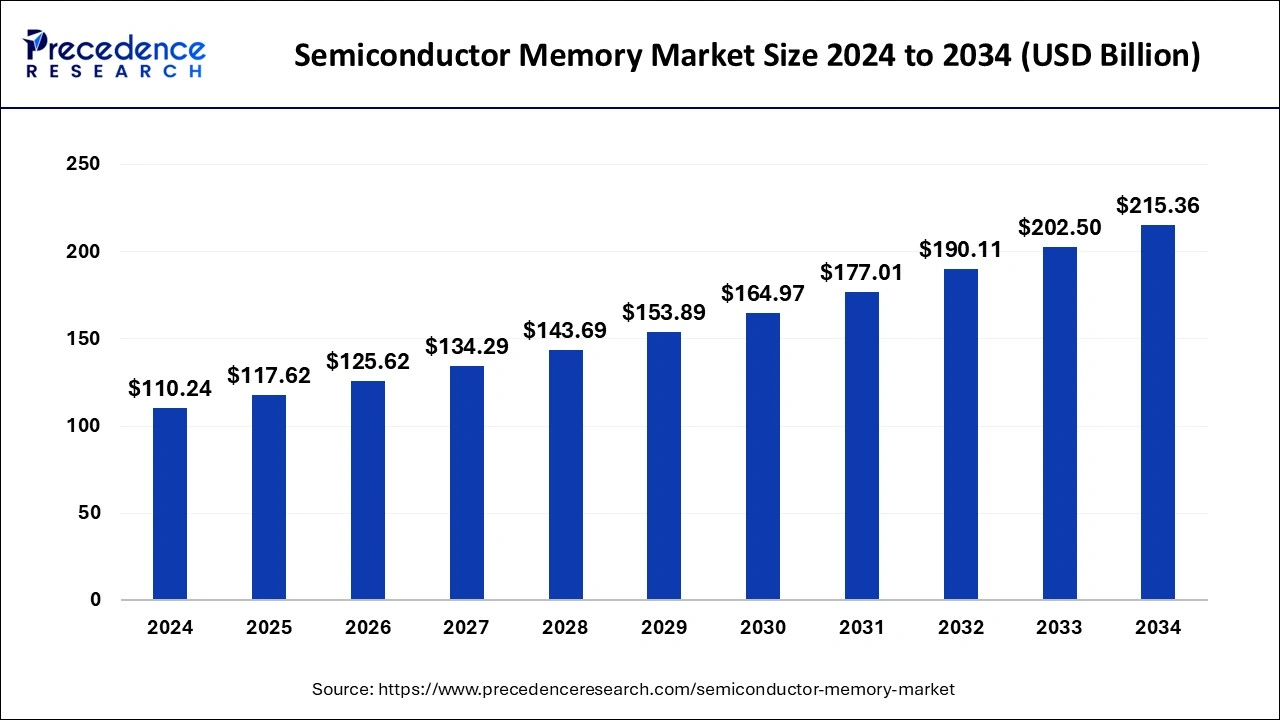

by The semiconductor memory market size was evaluated at USD 110.24 billion in 2024 and is predicted to reach around USD 215.36 billion by 2034 with a CAGR of 6.92%.

Get Sample Copy of Report@ https://www.precedenceresearch.com/sample/1080

Key Insights

- In 2024, Asia Pacific accounted for more than 45% of the total revenue share.

- North America is projected to grow at the fastest CAGR from 2024 to 2034.

- The Dynamic Random Access Memory (DRAM) segment dominated the market with a 45% share in 2024.

- The consumer electronics application segment held the largest share of 35% in 2024.

- The automotive application segment is expected to grow at the highest CAGR over the forecast period.

Market Insights

Drivers

The semiconductor memory market is primarily driven by the growing demand for high-performance storage solutions in consumer electronics, data centers, and automotive applications. The increasing adoption of smartphones, laptops, and IoT devices has created a surge in the need for faster and more efficient memory solutions such as DRAM and NAND flash. Additionally, advancements in artificial intelligence, cloud computing, and edge computing are pushing demand for higher-capacity memory solutions to handle massive data processing requirements. The rise of 5G technology is further accelerating the need for enhanced memory performance in connected devices.

Opportunities

The expansion of artificial intelligence, machine learning, and big data analytics is opening new growth opportunities in the semiconductor memory market. The increasing demand for autonomous vehicles and advanced driver-assistance systems (ADAS) is also boosting the need for high-speed, reliable memory solutions. Moreover, the transition to 3D NAND technology and emerging memory solutions such as MRAM and RRAM provide new possibilities for efficiency and storage density improvements. The rising trend of smart homes and industrial automation further contributes to the growth of the market.

Challenges

The semiconductor memory industry faces challenges related to supply chain disruptions, raw material shortages, and fluctuating semiconductor prices. High manufacturing costs and the complexity of developing advanced memory technologies like 3D NAND and next-generation DRAM can also pose barriers to market entry. Additionally, the cyclical nature of the semiconductor industry often leads to price volatility, impacting profitability for manufacturers. Increasing competition among major players is another challenge, as companies continuously strive to improve memory efficiency and reduce costs.

Regional Outlook

Asia Pacific dominates the semiconductor memory market, with leading manufacturing hubs in China, South Korea, and Taiwan. The region benefits from strong demand for consumer electronics and increasing investments in semiconductor fabrication plants. North America is experiencing rapid growth due to rising demand from data centers, AI applications, and cloud computing. Europe remains a significant player, focusing on automotive memory applications and research into next-generation memory technologies. Meanwhile, emerging markets in Latin America and the Middle East & Africa are gradually expanding their semiconductor capabilities to support growing digital infrastructure.

Semiconductor Memory Market Companies

- Micron Technology

- Integrated Silicon Solution Inc.

- Cypress Semiconductor Corporation

- Samsung Electronics

- Macronix International Co., Ltd.

- Taiwan Semiconductor

- SK Hynix

- Toshiba Corp.

- Texas Instruments

- IBM Corporation

Segments Covered in the Report

By Type

- Flash ROM

- MRAM

- SRAM

- DRAM

- Others

By Application

- IT & Telecommunication

- Medical

- Consumer Electronics

- Industrial

- Automotive

- Aerospace & Defense

- Others

By Geography

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Ready for more? Dive into the full experience on our website@ https://www.precedenceresearch.com/