by

by

Direct-to-Chip Liquid Cooling Market Key Points

-

North America dominated the global market with the largest market share of 40% in 2024.

-

The U.S. direct-to-chip liquid cooling market is expected to grow at a solid CAGR of 21.8% from 2025 to 2030.

-

Asia Pacific is projected to register the fastest CAGR of 22.7% during the forecast period.

-

By cooling solution type, the single-phase liquid cooling segment accounted for the highest market share of 66% in 2024.

-

The two-phase liquid cooling segment is anticipated to grow at the fastest rate during the forecast period.

-

By component cooling, the CPU cooling segment held the largest share of the market in 2024.

-

The memory cooling segment is projected to expand rapidly over the coming years.

-

By liquid coolant type, the water-based coolants segment contributed the highest market share in 2024.

-

The dielectric fluids segment is expected to witness the fastest growth during the projected timeframe.

-

By application, the data center segment dominated the market in 2024.

-

The high-performance computing (HPC) segment is expected to expand rapidly in the years ahead.

-

By end-use, the telecommunications segment held a significant market share in 2024.

-

The oil and gas segment is projected to experience the fastest CAGR throughout the forecast period.

Market Overview

The Direct-to-Chip (D2C) liquid cooling market is rapidly gaining prominence as data centers and high-performance computing (HPC) environments seek advanced thermal management solutions to combat rising heat loads. D2C liquid cooling involves the direct circulation of a coolant to a cold plate that sits atop the chip or processor. This technology offers more efficient heat removal than traditional air cooling, enabling greater computing density and performance while reducing overall energy consumption.

As computing power scales up—driven by AI workloads, cloud computing, edge deployments, and blockchain applications—traditional air-based systems are proving insufficient to handle the escalating thermal output. Direct-to-chip cooling emerges as a vital innovation, offering precise, localized, and scalable cooling solutions for servers, GPUs, and CPUs. The market is in transition from early-stage adoption to broader commercialization, fueled by hyperscalers, colocation data centers, government labs, and enterprise computing environments.

D2C cooling is increasingly seen as a cornerstone of sustainable and next-generation data center infrastructure. It not only reduces power usage effectiveness (PUE) but also allows data centers to operate at higher densities without compromising performance or uptime. This positions the technology at the heart of the future green computing ecosystem.

Growth Factors

Several factors are driving the robust growth of the D2C liquid cooling market. The most prominent is the explosive growth in data processing and computing demands, especially due to AI model training, 5G infrastructure, real-time analytics, and immersive applications such as AR/VR. These workloads generate massive amounts of heat that air-based systems cannot efficiently manage.

Increasing chip density and power consumption of modern CPUs and GPUs are accelerating the shift to more efficient thermal management. With processors surpassing 400–600 watts of thermal design power (TDP), D2C liquid cooling becomes essential to prevent thermal throttling and hardware degradation.

Another significant growth factor is the growing focus on energy efficiency and sustainability in the data center industry. With data centers accounting for an increasing share of global energy usage, operators are under pressure to lower power and water consumption. D2C cooling enables improved thermal efficiency, reducing the need for energy-intensive chillers and fans, and supports carbon reduction goals.

In addition, regulatory and corporate sustainability commitments are compelling data center operators to adopt innovative cooling technologies. Global hyperscale players like Google, Microsoft, and Meta are setting benchmarks for PUE and emissions reductions, thereby stimulating demand for liquid cooling systems.

Impact of AI on the Market

AI plays a multifaceted role in advancing the direct-to-chip liquid cooling market. At the infrastructure level, AI workloads are among the leading drivers of D2C adoption, as training large language models and neural networks requires high-density, power-hungry hardware configurations. These AI-driven systems generate heat loads far exceeding what conventional air cooling can handle, making liquid cooling essential for efficiency and performance.

Beyond being a catalyst for adoption, AI is also embedded in the optimization of D2C cooling systems. AI algorithms are used to dynamically manage coolant flow, temperature regulation, and heat distribution, adjusting in real time to workload fluctuations. This enables predictive and adaptive thermal management, extending component life and reducing energy waste.

AI also facilitates predictive maintenance of cooling infrastructure by analyzing sensor data to detect early signs of pump failure, fluid degradation, or flow obstruction. These predictive capabilities reduce downtime, improve system reliability, and optimize lifecycle costs.

Moreover, AI-enhanced digital twins of data centers can simulate thermal behavior under different workloads, enabling engineers to design and deploy more efficient D2C systems. These insights support smart data center automation where cooling is intelligently coordinated with workload management and power provisioning.

Market Scope

| Report Coverage | Details |

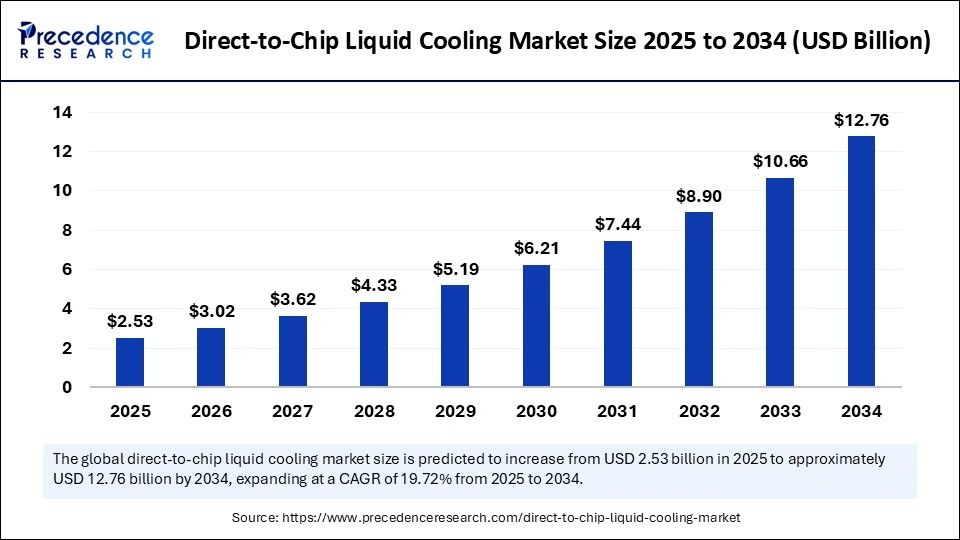

| Market Size by 2034 | USD 12.76 Billion |

| Market Size in 2025 | USD 2.53 Billion |

| Market Size in 2024 | USD 2.11 Billion |

| Market Growth Rate from 2025 to 2034 | CAGR of 19.72% |

| Dominating Region | North America |

| Fastest Growing Region | Asia Pacific |

| Base Year | 2024 |

| Forecast Period | 2025 to 2034 |

| Segments Covered | Cooling Solution Type, Component Cooling, Liquid Coolant Type, Application, End Use, and Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Market Drivers

The D2C liquid cooling market is propelled by several compelling drivers. Chief among them is the escalating thermal design power of modern computing components. As semiconductors become denser and more powerful, they generate unprecedented amounts of heat. D2C cooling delivers precise heat dissipation directly at the source, making it the most effective solution for next-gen computing environments.

Data center space constraints are another key driver. As real estate and operational costs rise, operators are striving to increase compute density per square foot. D2C systems allow tighter server packaging without the thermal penalties of air-cooled environments.

The rising cost of electricity and demand for sustainable operations are also motivating data center operators to seek more efficient cooling systems. D2C cooling significantly lowers fan use, supports higher inlet water temperatures, and facilitates heat reuse strategies, all of which contribute to lower total cost of ownership and environmental impact.

Industry support and ecosystem maturity are further accelerating adoption. The Open Compute Project (OCP), ASHRAE standards, and initiatives by OEMs and hyperscalers are promoting interoperability, standardization, and integration of D2C solutions into mainstream data center designs.

Opportunities

There are abundant opportunities in the D2C liquid cooling market, especially in emerging segments and geographies. One major opportunity is the integration of D2C cooling with edge computing and modular data centers, where space and environmental conditions limit the use of traditional HVAC systems. Compact, scalable D2C solutions offer a practical alternative for these environments.

Another opportunity lies in retrofit and hybrid deployments, where D2C cooling can be integrated into existing air-cooled facilities to enhance performance without a full infrastructure overhaul. These hybrid models allow gradual adoption and de-risk capital investments.

Geothermal and heat reuse applications also present opportunities. The heat removed by D2C systems can be recovered and repurposed for district heating or industrial processes, creating new value streams and supporting circular energy models.

Moreover, cross-industry expansion offers growth potential. Beyond data centers, D2C cooling is applicable in scientific computing, aerospace R&D, automotive testing, and defense simulation environments—anywhere high-intensity compute systems are used.

Challenges

Despite its advantages, the D2C market faces several challenges. One of the most significant is the high upfront cost and complexity of implementation. D2C systems require specialized plumbing, custom cold plates, and precise thermal designs, which can deter cost-sensitive operators.

Compatibility and standardization issues are another hurdle. Integrating D2C cooling across different server and chip architectures can be technically challenging, especially in heterogeneous environments. OEMs must collaborate to ensure interoperability and reliability across hardware vendors.

Maintenance and operational know-how are also barriers. Unlike traditional air cooling, liquid systems involve fluid handling, leak risk, and regular coolant management. This requires training and cultural shifts in data center operations.

Risk perception around fluid leakage and system reliability continues to slow adoption in some regions. While modern systems are robust and leak-proof, the psychological barrier remains for many operators accustomed to dry environments.

Finally, supply chain and availability of specialized components, such as cold plates and manifolds, can impact lead times and scalability, especially during global manufacturing disruptions.

Regional Outlook

North America is currently the largest market for D2C liquid cooling, led by the U.S., where hyperscalers, research labs, and government computing facilities are early adopters. Strong investment in AI, cloud infrastructure, and sustainability commitments make the region a hub for innovation and deployment.

Europe follows closely, driven by strict environmental regulations, high electricity costs, and ambitious climate goals. Countries like Germany, the Netherlands, and Sweden are leading adopters, integrating liquid cooling into their energy-efficient data center designs. The region also emphasizes heat reuse, where D2C systems can play a key role.

Asia-Pacific is the fastest-growing region, with China, Japan, South Korea, and Singapore leading the way. Rapid digitalization, 5G rollout, and AI R&D are boosting demand for high-performance computing infrastructure, making D2C cooling increasingly attractive.

Middle East and Africa, while nascent, hold potential due to extreme temperatures and growing interest in sustainable data centers. UAE and Saudi Arabia, in particular, are investing in smart cities and AI-driven infrastructure that may drive future D2C adoption.

Latin America is gradually embracing liquid cooling, particularly in urban hubs with expanding data infrastructure. Brazil and Mexico are seeing early interest as part of broader digital transformation and energy-efficiency initiatives.

Direct-to-Chip Liquid Cooling Market Companies

- ZutaCore

- Advanced Micro Devices, Inc.

- Schneider Electric

- JetCool Technologies

- LiquidStack

- Iceotope Technologies

- CoolIT Systems

- Asetek

- Fujitsu

- Chilldyne, Inc.

- Vertiv Holdings Co

Segment Covered in the Report

By Cooling Solution Type

- Single-phase liquid cooling

- Two-phase liquid cooling

By Component Cooling

- CPU cooling

- GPU cooling

- ASIC cooling

- Memory cooling

- Other

By Liquid Coolant Type

- Water-based coolants

- Dielectric fluids

- Mineral oils

- Engineered fluids

By Application

- Datacenter

- Workstations

- High-performance computing (HPC)

- Edge computing devices

- Supercomputers

- Others

By End Use

- Telecommunications

- Financial services

- Healthcare and life sciences

- Oil and gas

- Aerospace and defense

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Read Also: High Purity Quartz Market

Get this report to explore global market size, share, CAGR, and trends, featuring detailed segmental analysis and an insightful competitive landscape overview @ https://www.precedenceresearch.com/sample/6103

You can place an order or ask any questions, please feel free to contact at sales@precedenceresearch.com|+1 804 441 9344