by

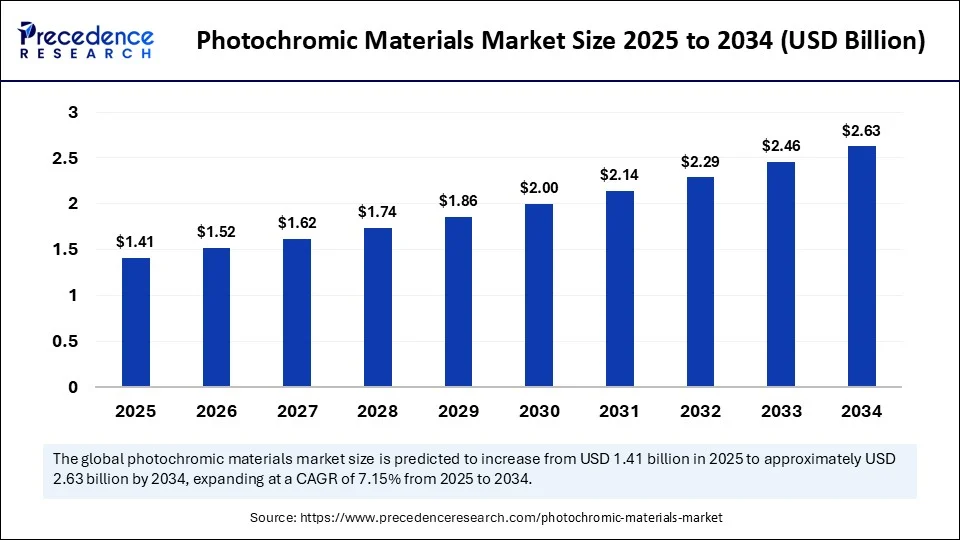

by The global photochromic materials market size is estimated to attain around USD 2.63 billion by 2034 increasing from USD 1.32 billion in 2024, with a CAGR of 7.15%

Growth is driven by persistent demand for photochromic ophthalmic lenses, broadening use in fashion and technical textiles, and rapid adoption in security printing, packaging, and building façades where dynamic tinting improves aesthetics and energy efficiency. North America currently holds the lion’s share of revenue on the back of mature eyewear and printing industries, while Europe maintains strong momentum through architectural glazing innovations. Asia‑Pacific is emerging as the fastest‑growing region, fueled by expanding middle‑class demand for adaptive sunglasses, booming textile exports, and government incentives for energy‑smart buildings.

Photochromic Materials Market Key Points

-

The global photochromic materials market was valued at USD 1.32 billion in 2024.

-

It is projected to reach approximately USD 2.63 billion by 2034, growing at a CAGR of 7.15% from 2025 to 2034.

-

North America led the market in 2024, accounting for the largest share of 42%.

-

The Asia Pacific region is expected to grow at a notable CAGR throughout the forecast period.

-

Among material types, inorganic photochromic materials dominated the market in 2024, holding a 63% share.

-

The organic photochromic materials segment is forecasted to expand at the fastest CAGR between 2025 and 2034.

-

By application, the eyewear segment held the largest share of 74% in 2024.

-

The smart windows and films segment is projected to witness significant growth during the forecast years.

-

Based on end users, the consumer segment was the top contributor in 2024, with a 71% share.

-

The construction and architecture segment is expected to register a strong CAGR over the forecast period.

-

Regarding activation mechanisms, the UV-activated segment held the largest market share of 81% in 2024.

-

The dual light-activated (UV + visible) segment is anticipated to grow at a noteworthy CAGR from 2025 to 2034.

Photochromic Materials Market Growth Factors

Multiple structural forces underpin market expansion. First, rising awareness of ultraviolet (UV) eye protection and increasing rates of myopia are fueling global demand for adaptive lenses that seamlessly shift tint outdoors, offering both convenience and medical benefits. Second, fashion and sportswear brands are embracing color‑shifting yarns and inks to create interactive garments that respond to sunlight, generating fresh consumer excitement and premium price points. Third, the packaging industry is exploiting photochromic labels as tamper‑evident seals and cold‑chain freshness indicators, strengthening supply‑chain accountability.

Fourth, evolving building‑energy codes are pushing architects toward dynamic shading glass that reduces HVAC loads; photochromic interlayers or coatings offer a passive, power‑free alternative to electrochromic windows. Finally, continual cost reductions in microencapsulation and polymer‑matrix technology are lowering barriers for brand owners who previously viewed photochromics as expensive specialty additives.

Role of AI in the Photochromic Materials Market

Artificial intelligence is increasingly integral to photochromic‑materials innovation and manufacturing. Machine‑learning models trained on molecular‑structure databases now predict new chromophore backbones with faster switching speeds, higher fatigue resistance, and broader visible‑light activation ranges—dramatically shortening discovery cycles. In process development, AI‑driven reactors monitor temperature, pH, and solvent concentration in real time, autonomously adjusting parameters to maximize yield and color‑density consistency.

Predictive analytics also inform supply‑chain planning: by ingesting regional UV‑index data, eyewear retailers can optimize inventory of light‑adaptive lenses for different latitudes and seasons. Downstream, AI‑powered computer vision embedded in packaging lines validates the activation performance of photochromic inks, ensuring product security without manual sampling. As connected “smart” garments gain traction, fabric‑integrated sensors coupled with AI could one day modulate photochromic response based on wearer location, UV exposure history, or stylistic preferences.

Photochromic Materials Market Scope

| Report Coverage | Details |

| Market Size by 2034 | USD 2.63 Billion |

| Market Size in 2025 | USD 1.41 Billion |

| Market Size in 2024 | USD 1.32 Billion |

| Market Growth Rate from 2025 to 2034 | CAGR of 7.15% |

| Dominating Region | North America |

| Fastest Growing Region | Asia Pacific |

| Base Year | 2024 |

| Forecast Period | 2025 to 2034 |

| Segments Covered | Type of Material, Application, End User, Activation Mechanism, and Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Market Drivers

Day‑to‑day momentum comes from surging consumer interest in multi‑functionality and personalization. Photochromic lenses eliminate the need to switch between prescription and sunglasses, a value proposition that resonates strongly with urban consumers seeking convenience. Outdoor apparel brands differentiate their lines with dynamic prints that reveal graphics under sunlight, capturing social‑media attention and boosting unit sales. On the industrial side, regulators and brand owners are mandating anti‑counterfeit measures in pharmaceuticals and luxury goods; photochromic security inks meet this need while remaining invisible under normal light conditions.

Furthermore, the global push to curb building‑sector energy consumption is encouraging adoption of passive, adaptive glazing technologies that rely on photochromic coatings rather than wiring and electronics, reducing installation complexity. Together, these customer expectations, regulatory trends, and environmental goals sustain a healthy pipeline of new applications and consistent procurement contracts.

Opportunities

Ample white space exists for innovators capable of pushing performance and cost boundaries. The development of visible‑light‑activated and near‑infrared‑activated photochromics opens opportunities for indoor color‑change features in consumer electronics or retail displays where UV light is absent. Integration with 3‑D‑printing resins enables rapid prototyping of custom, color‑shifting parts for automotive dashboards, aerospace cabin interiors, and interactive toys. In healthcare, photochromic dermal patches could visually signal excessive UV exposure, supporting skin‑cancer prevention campaigns.

Agricultural films that modulate shading according to sunlight intensity promise water and energy savings in greenhouses. Finally, as circular‑economy principles gain traction, companies that engineer recyclable or biodegradable photochromic systems—replacing traditional spiropyrans with naturally sourced fulgides or donor–acceptor Stenhouse adducts—stand to capture sustainability‑conscious buyers and comply with tightening chemical regulations.

Challenges

Despite strong tailwinds, the market faces hurdles around durability, environmental compliance, and cost. Fatigue—loss of switching performance after repeated cycles—remains a technical challenge, especially in textile and façade applications exposed to harsh weather. Many traditional photochromic chemicals contain halogens or metal complexes that are under increasing regulatory scrutiny; reformulating to meet REACH and TSCA guidelines can raise R&D costs.

Manufacturing scale‑up requires strict control of microencapsulation particle size to prevent speckling or uneven tint, necessitating capital‑intensive equipment. Price sensitivity in emerging markets, where single‑vision lenses dominate, can limit adoption of premium photochromic coatings. Moreover, intellectual‑property barriers are significant; leading chemical conglomerates hold extensive patent portfolios, making entry more difficult for smaller companies without cross‑licensing agreements.

Photochromic Materials Market Regional Outlook

North America maintains the largest revenue share thanks to its strong eyewear brands, high disposable income, and widespread acceptance of adaptive lenses. Energy‑efficiency incentives further drive architectural glazing projects.

Europe benefits from stringent sustainability regulations and fashion houses that experiment with color‑shifting fabrics, though economic headwinds may temper short‑term growth.

Asia‑Pacific is poised for the fastest CAGR, propelled by rising middle‑class consumption in China and India, aggressive retail expansion in Southeast Asia, and government‑backed energy‑saving initiatives in Japan and South Korea.

Latin America shows moderate but rising demand, particularly in Brazil’s sportswear sector,

The Middle East & Africa are gradually adopting photochromic materials in luxury retail packaging and high‑sunlight building façades, with tourism and hospitality projects providing pockets of growth.

Segmental Insights

-

By Material Type: Organic photochromic dyes, such as spiropyrans and naphthopyrans, dominate revenue owing to their vibrant color range and tunable activation spectra. However, inorganic oxides and hybrid nanocomposites are gaining share due to superior UV durability and thermal stability, making them suitable for long‑life architectural and automotive glazing.

-

By Application: Ophthalmic lenses remain the largest application segment, accounting for well over half of global consumption in 2024. Textiles and apparel represent the fastest‑growing application as athleisure and outdoor brands exploit dynamic prints. Security and packaging follow closely, driven by anti‑counterfeiting and freshness‑indicator uses in pharmaceuticals and food.

-

By End‑Use Industry: The consumer goods sector leads overall demand, primarily through eyewear and apparel. The construction industry is expanding quickly due to dynamic façade coatings, while printing and packaging show steady growth linked to product security innovations.

By Distribution Channel: OEM agreements with lens manufacturers and textile mills command the highest share, ensuring consistent volume flows. Specialty chemical distributors are the fastest‑growing channel, supplying small and mid‑size printers, textile converters, and niche packaging firms that demand flexible batch sizes.

Photochromic Materials Market Companies

- Transitions Optical (EssilorLuxottica)

- Tokuyama Corporation

- Mitsui Chemicals

- PPG Industries

- Nissan Chemical Corporation

- Schott AG

- Vision Ease

- Color Change Corporation

- Chromatic Technologies Inc. (CTI)

- Milliken Chemical

Read Also: Direct-to-Chip Liquid Cooling Market

You can place an order or ask any questions, please feel free to contact at sales@precedenceresearch.com |+1 804 441 9344