by

by What is the projected market size and growth rate of the Venous Leg Ulcer market from 2025 to 2034?

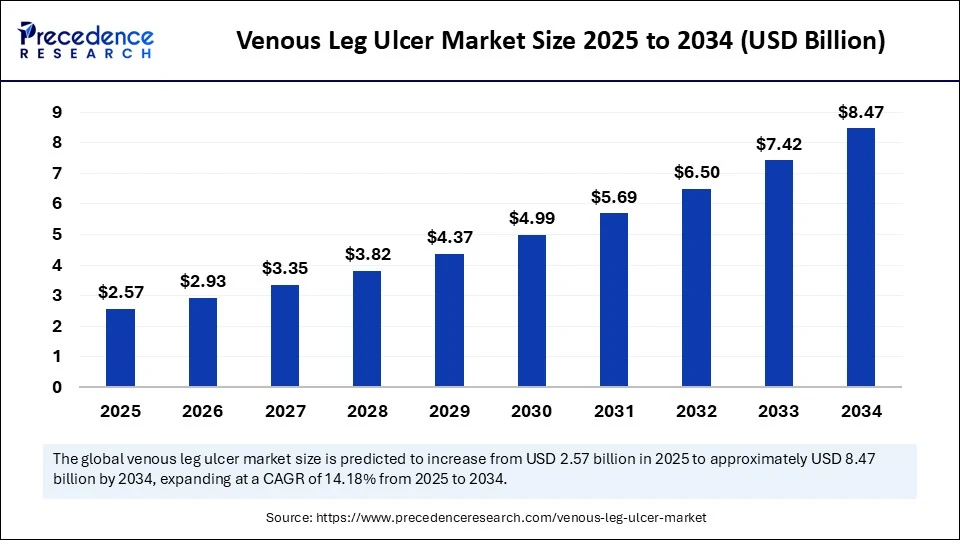

Venous Leg Ulcer Market Key Insights

-

The global venous leg ulcer market was valued at USD 2.25 billion in 2024 and is forecast to reach USD 8.47 billion by 2034, registering a strong CAGR of 14.18% from 2025 to 2034.

-

North America led the global market in 2024, accounting for the largest share of 37%, while the Asia Pacific region is projected to expand at a notable growth rate during the forecast period.

-

By treatment type, compression therapy dominated the market with a 40% share in 2024. However, the active wound care segment is poised to grow at the fastest CAGR in the coming years.

-

Based on ulcer stage, uncomplicated/initial VLUs represented the largest segment with a 45% share in 2024, while the infected/recurrent VLU segment is expected to grow rapidly over the forecast timeline.

-

In terms of end users, hospitals accounted for the major market share of 50% in 2024, whereas ambulatory surgical centers are projected to experience the highest CAGR between 2025 and 2034.

-

By distribution channel, direct tenders held the dominant 60% share in 2024, while online pharmacies are anticipated to witness significant growth throughout the forecast period.

How is Artificial Intelligence transforming the VLU market?

Artificial Intelligence (AI) is increasingly being used to improve the diagnosis and monitoring of venous leg ulcers. AI-based imaging tools and wound measurement systems assist clinicians in assessing wound dimensions, depth, tissue type, and healing progression with precision. These platforms help standardize assessments, enhance documentation for reimbursement, and allow for more objective comparisons during follow-ups. AI can also identify patterns in wound deterioration, thereby enabling earlier interventions and more informed decision-making.

Beyond diagnostics, AI plays a pivotal role in personalized treatment planning and remote monitoring. Predictive analytics tools can estimate healing times based on comorbidities, wound stage, and patient lifestyle, helping clinicians optimize care pathways. Furthermore, AI-integrated mobile apps now enable real-time monitoring and alerts for wound complications, improving patient engagement and adherence, especially among elderly or home-bound individuals.

How is the U.S. market contributing to global VLU growth?

The U.S. venous leg ulcer market size was valued at USD 582.75 million in 2024 and is projected to be reacharound USD 2,239.26 million by 2034, growing at a CAGR of 14.41% from 2025 to 2034.

This growth is largely supported by the country’s aging population, with over 56 million Americans aged 65 and older. The U.S. also faces high rates of obesity and diabetes, both major contributors to venous insufficiency and ulcer formation. Additionally, strong support from Medicare and Medicaid, along with active wound care research programs and clinical trials, is accelerating adoption of advanced treatment solutions.

Why does North America lead the Venous Leg Ulcer market?

North America continues to dominate the VLU market, owing to its well-established healthcare systems, advanced wound care technologies, and supportive reimbursement models. The region is home to several major wound care manufacturers and benefits from early adoption of technologies like AI-enabled imaging, NPWT, and skin substitutes. Furthermore, there is heightened awareness among both patients and providers, leading to early diagnosis and intervention. Hospital infrastructure in the region also enables effective multidisciplinary treatment approaches, from vascular surgery to home wound management.

Why is Asia Pacific the fastest-growing region for VLU treatment?

Asia Pacific is projected to grow at the fastest rate in the global VLU market, driven by increasing rates of diabetes, obesity, and sedentary lifestyles, especially in urbanized regions. Rapid healthcare infrastructure development in countries like India, China, and Southeast Asia is also improving access to chronic wound care services. Furthermore, the growing middle-class population, increased government healthcare investments, and expansion of telemedicine and mobile health platforms are key contributors to the region’s growth. Medical tourism in APAC is also creating demand for advanced yet affordable wound care solutions.

What is Europe’s position in the global VLU market?

Europe maintains a strong position in the global VLU market due to its aging population—over 20% of EU citizens are aged 65 or older—and a well-regulated, innovation-driven healthcare ecosystem. The region has witnessed significant investment in biologic wound healing, tissue engineering, and R&D of advanced wound care products. Governments in countries like Germany, France, and the UK support chronic wound management through public health initiatives and reimbursement policies. Furthermore, telehealth platforms are increasingly being used to extend specialized care to rural or aging populations.

What market potential exists in Latin America and the Middle East & Africa?

In Latin America, the VLU market is expanding due to improved access to healthcare services, increasing awareness about chronic wound management, and growth in the prevalence of diabetes and vascular conditions. Countries such as Brazil, Mexico, and Argentina are investing in basic wound care products and infrastructure, particularly in urban hospitals and private healthcare systems.

Meanwhile, the Middle East & Africa (MEA) region is witnessing gradual adoption of modern wound care technologies, driven by an increase in chronic disease prevalence, particularly diabetes. Growth is further supported by rising healthcare budgets and the presence of international aid programs. However, affordability and access remain major challenges, making this a market with untapped long-term potential.

What are the key trends shaping the future of the VLU market?

-

The growing elderly population is increasing the prevalence of VLUs

-

Advanced wound healing technologies like NPWT and bioengineered skin are gaining traction

-

Telemedicine and mobile wound monitoring apps are reshaping care delivery

-

Rising healthcare expenditure in emerging countries is expanding access to modern treatments

-

Focus on improving quality of life and reducing hospital stays is promoting long-term care models

Venous Leg Ulcer Market Scope

| Report Coverage | Details |

| Market Size by 2034 | USD 8.47 Billion |

| Market Size in 2025 | USD 2.57 Billion |

| Market Size in 2024 | USD 2.25 Billion |

| Market Growth Rate from 2025 to 2034 | CAGR of 14.18% |

| Dominating Region | North America |

| Fastest Growing Region | Asia Pacific |

| Base Year | 2024 |

| Forecast Period | 2025 to 2034 |

| Segments Covered | Treatment Type, Ulcer Stage, End User, Distribution Channel, and Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Venous Leg Ulcer Market Dynamics

Drivers:

The market is driven by the global aging trend, as older adults are at greater risk of venous disease and chronic ulcers. Coupled with the increasing incidence of obesity and diabetes, this is creating a growing patient pool. Technological advancements, including AI-powered diagnostics, portable NPWT devices, and innovative dressings, are also improving healing rates and patient outcomes.

Restraints:

Despite these opportunities, high costs of advanced wound care solutions remain a major barrier, particularly in price-sensitive markets. Limited awareness in rural and underdeveloped regions, as well as low patient adherence to compression therapy, also constrain treatment effectiveness and market reach.

Opportunities:

Emerging markets offer vast opportunities for expansion, especially with increasing government investments in chronic disease management. Moreover, home healthcare and remote monitoring platforms are opening new avenues for personalized wound care, especially for elderly patients in non-clinical settings. Development of next-generation wound care products using regenerative technologies is expected to shape the future of VLU treatment.

How is the market segmented, and what are the key insights for each category?

By Treatment Type:

Compression therapy is the most widely adopted method, particularly in early-stage ulcers. Advanced wound dressings and NPWT devices are used in hospital settings, while bioengineered substitutes are emerging for complex, non-healing wounds.

By Stage/Severity:

VLUs are typically segmented by early, moderate, and severe stages. Early-stage ulcers are often managed in outpatient clinics, while severe cases may require surgical intervention, skin grafts, or hospitalization.

By End User:

Hospitals remain the largest end-user due to the complex care required. However, home healthcare and outpatient centers are rapidly growing as patients seek convenience and continuity of care.

By Distribution Channel:

Hospital pharmacies and specialty clinics dominate the advanced treatment product market. E-commerce and retail pharmacies are becoming vital for compression garments and basic wound dressings.

Companies are leading the Venous Leg Ulcer market

-

Smith & Nephew

-

3M Health Care

-

ConvaTec Group plc

-

Mölnlycke Health Care AB

-

Coloplast A/S

-

Organogenesis Holdings

-

Integra LifeSciences

-

B. Braun Melsungen

-

Cardinal Health

-

Medline Industries

-

MiMedx Group

-

Kerecis

-

Urgo Medical

-

Derma Sciences

-

Advancis Medical

What are the recent developments in the VLU market?

-

April 2024 – Organogenesis reported favorable Phase III trial results for PuraPly MZ, a bioengineered skin product.

-

January 2024 – 3M Health Care launched a compression system specifically designed for elderly patients with VLUs.

-

October 2023 – Smith & Nephew introduced a smart wound dressing with real-time monitoring sensors.

-

August 2023 – Coloplast acquired Kerecis to boost its regenerative wound healing capabilities.

-

May 2023 – ConvaTec released a mobile wound documentation tool for clinics and home health providers.

Segments are covered in the report

By Treatment Type:

-

Compression Therapy

-

Advanced Wound Dressings

-

NPWT

-

Bioengineered Skin Substitutes

-

Debridement Devices

By Stage/Severity:

-

Early Ulcers

-

Moderate Ulcers

-

Severe/Non-healing Ulcers

By End User:

-

Hospitals

-

Specialty Wound Clinics

-

Home Healthcare

-

Ambulatory Surgical Centers

By Distribution Channel:

-

Hospital & Retail Pharmacies

-

E-commerce

-

Homecare Providers

By Region:

-

North America

-

Europe

-

Asia Pacific

-

Latin America

-

Middle East & Africa

Read Also: Pharmacovigilance and Drug Safety Software Market

You can place an order or ask any questions, please feel free to contact at sales@precedenceresearch.com|+1 804 441 9344