by

by

Power SCADA (Supervisory Control and Data Acquisition) Market Key Points

-

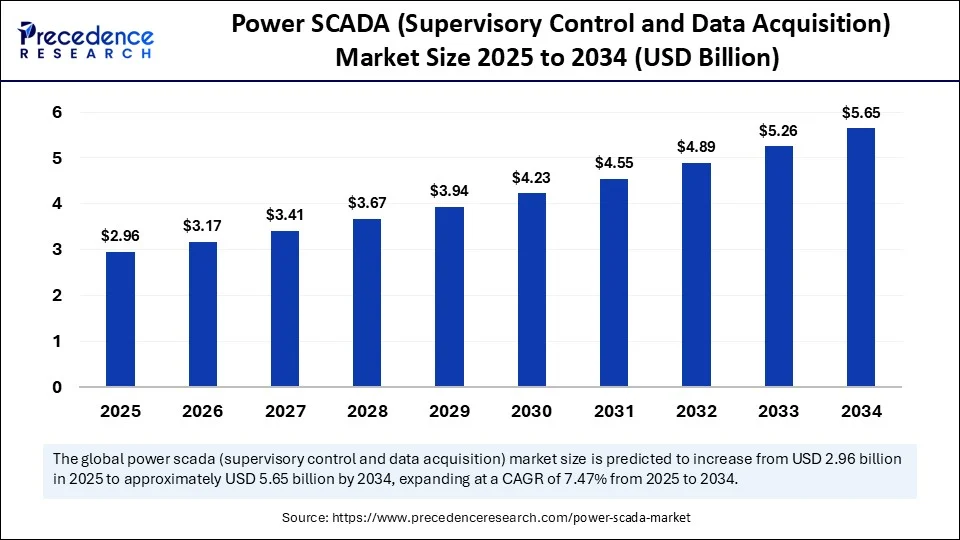

The global power SCADA market was valued at USD 2.75 billion in 2024.

-

It is anticipated to reach around USD 5.65 billion by 2034, growing at a CAGR of 7.47% from 2025 to 2034.

-

North America led the market in 2024, accounting for the largest share of 42%.

-

The Asia Pacific region is projected to grow at the fastest CAGR over the forecast period.

-

Among components, the hardware segment held the largest market share in 2024.

-

The software segment is expected to witness the highest growth rate during the forecast years.

-

Based on architecture, the open system architecture (OSA) segment dominated the market in 2024.

-

The closed system architecture segment is forecasted to expand at the fastest CAGR in the upcoming years.

-

By deployment model, the on-premises segment held the highest share in 2024.

-

The cloud-based deployment model is emerging as the fastest growing segment over the forecast period.

-

In terms of end-use industry, power generation was the leading segment in 2024.

-

The non-renewables segment is projected to be the fastest-growing end-use industry in the years ahead.

Power SCADA Market Growth Factors

Several structural trends underpin this expansion. First, the global push to decarbonize electricity is accelerating wind, solar, and battery deployments—assets that require high‑speed, data‑rich SCADA oversight to coordinate intermittency and ramp rates. Second, booming industrial automation and smart‑factory initiatives are driving private microgrids and captive power plants to install advanced SCADA suites for energy‑cost optimization and downtime reduction.

Governments are allocating large stimulus packages to grid‑modernization programs—upgrading transmission, distribution, and substation infrastructure with condition‑based monitoring that feeds directly into SCADA environments. Finally, falling costs of edge sensors, industrial IoT gateways, and high‑bandwidth communications are lowering the threshold for smaller utilities and cooperatives to adopt full‑featured systems.

Role of AI in the Power SCADA Market

Artificial intelligence is rapidly transforming SCADA from a reactive monitoring framework into a predictive, self‑optimizing brain for the power network. Machine‑learning engines embedded in SCADA analytics modules now forecast load, detect equipment anomalies, and identify evolving cyber threats within milliseconds. AI‑driven asset‑health models interpret vibration, temperature, and partial‑discharge data from transformers and circuit breakers, automatically scheduling maintenance before failures occur.

On the control side, reinforcement‑learning algorithms are beginning to fine‑tune voltage‑VAR optimization and economic dispatch of distributed generators, squeezing extra efficiency out of aging infrastructure. These advances not only cut operating costs and outage minutes, they also free human operators to focus on higher‑level decision‑making during grid emergencies.

Market Drivers

The market’s day‑to‑day momentum is powered by the need for real‑time situational awareness, rising cybersecurity requirements, and widening gaps between generation and load in fast‑growing economies. Utilities face regulatory directives to reduce System Average Interruption Duration Index (SAIDI) and report near‑instant fault locations—demands that only a robust SCADA platform can meet.

Meanwhile, cyber‑hardening mandates are pushing asset owners to migrate from legacy proprietary protocols to secure, encrypted architectures, triggering refresh cycles of hardware, software, and network infrastructure. In parallel, growing urbanization and electrification of transport place stress on aging grids, compelling utilities to invest in centralized and distributed SCADA nodes for improved load management and outage restoration.

Opportunities

Significant upside remains in cloud‑hosted SCADA deployments that deliver elastic compute power and advanced analytics to smaller utilities without extensive IT staff. Edge‑native SCADA modules, capable of autonomous micro‑decision‑making at substations and renewable plants, present another high‑growth niche as latency‑sensitive applications proliferate. Hydrogen electrolyzers and utility‑scale battery farms—assets now rolling out to balance renewable variability—require dedicated SCADA interfaces, opening white space for vendors that can supply industry‑specific templates. Emerging markets in Africa and Southeast Asia, which are leapfrogging to digital substations, offer greenfield prospects for turnkey SCADA solutions bundled with training and cyber‑security services.

Challenges

Despite strong tailwinds, the sector faces acute hurdles. Integrating heterogeneous legacy devices that use outdated protocols (e.g., Modbus RTU, IEC 60870‑5‑101) with modern IP‑based SCADA systems can be costly and risky. Cybersecurity vulnerabilities remain a moving target, with ransomware and state‑sponsored attacks focusing on critical infrastructure; maintaining continuous compliance with evolving NERC CIP, IEC 62443, and local standards strains utility budgets. Skilled workforce shortages in OT cybersecurity and SCADA engineering complicate large‑scale rollouts, while high upfront capital costs can delay procurement decisions, particularly for small municipal utilities. Lastly, interoperability across vendor ecosystems is not yet seamless, sometimes locking operators into proprietary platforms and slowing innovation.

Market Scope

| Report Coverage | Details |

| Market Size by 2034 | USD 5.65 Billion |

| Market Size in 2025 | USD 2.96 Billion |

| Market Size in 2024 | USD 2.75 Billion |

| Market Growth Rate from 2025 to 2034 | CAGR of 7.47% |

| Dominating Region | North America |

| Fastest Growing Region | Asia Pacific |

| Base Year | 2024 |

| Forecast Period | 2025 to 2034 |

| Segments Covered | Component, Architecture, Deployment Model, End-Use Industry, and Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Power SCADA Market Regional Outlook

North America currently commands the largest share—about 42 % of global revenue—thanks to its entrenched smart‑grid programs, early adoption of advanced distribution management, and federal funding aimed at grid resilience.

Europe follows closely, propelled by stringent renewable‑integration targets, widespread substation‑automation retrofits, and aggressive cybersecurity regulations.

Asia‑Pacific is expected to post the fastest CAGR through 2034, as China and India build out ultra‑high‑voltage transmission corridors and Southeast Asian nations modernize distribution networks to accommodate rapid urbanization.

Latin America is gradually upgrading hydro‑dominated grids and installing SCADA for cross‑border interconnections,

The Middle East & Africa focus on integrating solar megaprojects and enhancing reliability for energy‑intensive industries, creating pockets of rapid adoption despite budget constraints.

Power SCADA Market Segmental Insights

-

By Component – Hardware (RTUs, PLCs, communication infrastructure, HMI panels) generated the largest share in 2024, reflecting ongoing substation digitization, but software and analytics are growing fastest as utilities shift from data acquisition to real‑time intelligence and AI‑driven control.

-

By Architecture – Open‑system architectures (OSA) lead today’s deployments, prized for interoperability across multi‑vendor devices, while closed systems still serve niche high‑security environments and are projected to see incremental growth as certain operators prioritize air‑gapped solutions.

-

By Deployment Model – On‑premises SCADA remains dominant owing to data‑sovereignty concerns and critical‑infrastructure regulations, yet cloud‑based and hybrid models are the fastest‑rising segment, driven by cost advantages, rapid scalability, and seamless patch management.

-

By End‑Use Industry – Power generation—particularly gas, coal, and nuclear plants—captures the largest revenue share, relying on SCADA for turbine and boiler control, but renewable‑energy assets and microgrids represent the highest‑growth slice as nations accelerate clean‑energy targets.

-

By Region – North America sets the pace, Europe maintains solid adoption thanks to grid harmonization projects, Asia‑Pacific posts the steepest growth curve, and emerging regions leverage concessional financing to deploy SCADA in grid‑extension and interconnection projects.

Power SCADA Market Companies

- Siemens AG

- ABB Ltd.

- Schneider Electric SE

- General Electric Company

- Emerson Electric Co.

- Eaton Corporation plc

- Mitsubishi Electric Corporation

- Honeywell International Inc.

- Rockwell Automation, Inc.

- Hitachi Energy

- Toshiba Corporation

- Yokogawa Electric Corporation

- Larsen & Toubro Limited

- Open Systems International (OSI)

- Indra Sistemas S.A.

- ETAP (Operation Technology Inc.)

- ZIV Automation

- Ingeteam

- SCADAfence

- Advantech Co., Ltd.

Read Also: Photochromic Materials Market

You can place an order or ask any questions, please feel free to contact at sales@precedenceresearch.com |+1 804 441 9344