by

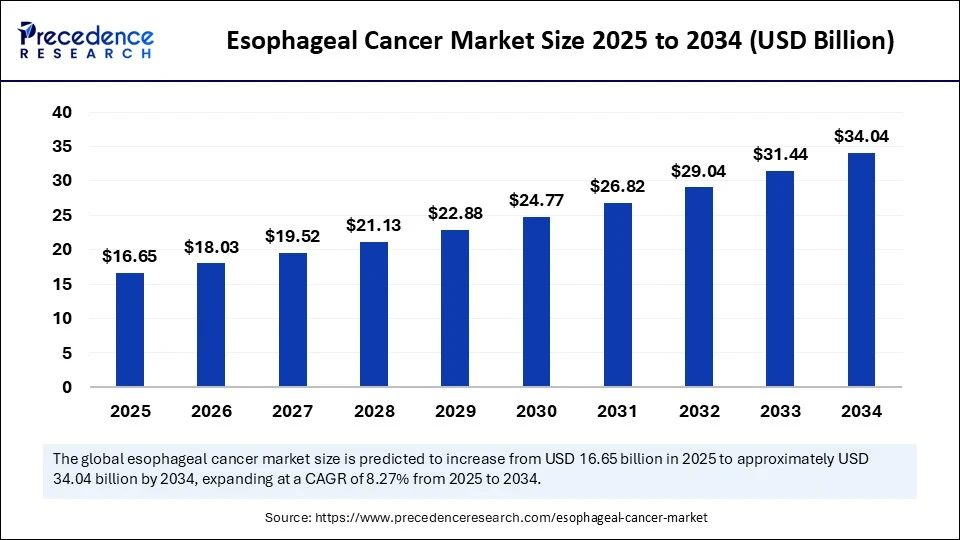

by The global esophageal cancer market size is estimated to climb around USD 34.04 billion by 2034 increasing from USD 15.38 billion in 2024, with a CAGR of 8.27%.

Get this report to explore global market size, share, CAGR, and trends, featuring detailed segmental analysis and an insightful competitive landscape overview @ https://www.precedenceresearch.com/sample/6348

-

North America dominated the esophageal cancer market in 2024, holding the largest market share of 40%.

-

Asia Pacific is projected to witness the fastest growth during the forecast period.

-

By cancer type:

-

Squamous cell carcinoma led the market with an 80% share in 2024.

-

Adenocarcinoma is expected to show significant growth over the forecast years.

-

-

By diagnosis:

-

Endoscopy accounted for a 40% market share in 2024.

-

The imaging segment is anticipated to grow substantially during the forecast period.

-

-

By treatment type:

-

Therapy-based treatments contributed the highest share of 60% in 2024.

-

-

By stage:

-

Stage II esophageal cancer held a notable market share of 35% in 2024.

-

-

By route of administration:

-

Intravenous treatments dominated with an 85% share in 2024.

-

Oral treatments are expected to grow notably in the coming years.

-

-

By end user:

-

Hospitals were the major end users, capturing 70% of the market in 2024.

-

Ambulatory surgical centers are forecasted to grow at a considerable rate.

-

-

By distribution channel:

-

Hospital pharmacies led the segment with a 60% market share in 2024.

-

Online pharmacies are projected to experience significant growth in the forecast period.

-

Esophageal Cancer Market Growth Factors

Several factors contribute to the robust growth of the esophageal cancer market. One of the primary growth drivers is the increasing prevalence of risk factors such as gastroesophageal reflux disease (GERD), obesity, smoking, alcohol use, and dietary habits, all of which are strongly associated with the development of esophageal cancer. Furthermore, the aging global population contributes to the increased risk of cancer, including esophageal malignancies.

Advances in diagnostics, including endoscopic techniques, PET-CT imaging, and molecular biomarker testing, are improving early detection rates. Additionally, rising healthcare expenditure, government support for oncology research, and better access to specialty care in developing economies are helping expand treatment coverage and improve patient outcomes.

Regional Outlook

The regional outlook for the esophageal cancer market is shaped by differences in disease prevalence, healthcare infrastructure, and innovation adoption.

North America dominates the market due to high healthcare expenditure, advanced oncology infrastructure, and a high rate of targeted therapy usage. The presence of key pharmaceutical companies and active research initiatives further supports growth in the region.

Europe follows closely, with countries like Germany, the UK, and France leading in the integration of advanced diagnostic technologies and clinical trials for esophageal cancer.

Asia-Pacific is projected to be the fastest-growing region owing to a higher incidence of squamous cell carcinoma, especially in China, Japan, and parts of Southeast Asia. Rapid improvements in healthcare access, investment in cancer care, and local production of biologics contribute to regional momentum.

Latin America, the Middle East, and Africa are showing gradual progress, but these regions face infrastructure and affordability limitations. However, international partnerships and government-supported cancer programs may help bridge the gap over time.

Role of AI in the Esophageal Cancer Market

Artificial intelligence (AI) is beginning to play a transformative role in the esophageal cancer market, particularly in diagnostics and clinical decision-making. AI algorithms, particularly deep learning models, are being developed to assist in interpreting endoscopic images to detect early-stage lesions that may be missed by the human eye. These technologies enhance the accuracy and speed of diagnosis, allowing for earlier intervention and potentially improved survival rates.

AI-powered platforms are being used to integrate histopathological, genomic, and clinical data to help oncologists tailor personalized treatment plans for individual patients. In the field of drug development, machine learning tools are being applied to accelerate the discovery of novel therapeutic agents and predict response rates to targeted therapies. As these technologies mature, AI is expected to become a core component in managing esophageal cancer more efficiently and effectively.

Esophageal Cancer Market Scope

| Report Coverage | Details |

| Market Size by 2034 | USD 34.04 Billion |

| Market Size in 2025 | USD 16.65 Billion |

| Market Size in 2024 | USD 15.38 Billion |

| Market Growth Rate from 2025 to 2034 | CAGR of 8.27% |

| Dominating Region | North America |

| Fastest Growing Region | Asia Pacific |

| Base Year | 2024 |

| Forecast Period | 2025 to 2034 |

| Segments Covered | Cancer Type, Diagnosis, Treatment, Stage, Route of Administration, End User, Distribution Channel and Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Esophageal Cancer Market Drivers

The esophageal cancer market is being driven by a combination of clinical needs and technological advancements. The growing burden of late-stage esophageal cancer, which requires intensive treatment, is propelling demand for innovative therapies and surgical interventions. The emergence of targeted therapies, including monoclonal antibodies against HER2 (e.g., trastuzumab) and immune checkpoint inhibitors (e.g., nivolumab, pembrolizumab), has opened new treatment pathways, especially for patients with advanced or metastatic disease.

Regulatory bodies are increasingly approving these drugs for broader indications, further boosting their adoption. Moreover, a better understanding of tumor biology and molecular subtypes is guiding more precise treatments. Additionally, the expansion of cancer screening programs in high-risk regions and the integration of esophageal cancer screening into general oncology care protocols are contributing to early detection and improving survival outcomes.

Opportunities

The esophageal cancer market offers numerous opportunities for growth and innovation. One major opportunity lies in the development of minimally invasive diagnostic and treatment solutions, such as robotic-assisted surgery and endoscopic therapies that reduce recovery times and hospital stays. The integration of telemedicine and digital health tools into oncology workflows also offers a scalable solution for follow-up care, remote diagnostics, and patient monitoring, especially in underserved regions.

The use of companion diagnostics to identify suitable candidates for targeted and immunotherapies is another promising area, enabling a shift toward more personalized oncology care. Moreover, pharmaceutical companies and biotech firms have the opportunity to expand clinical trials for novel therapeutics, especially in regions with rising incidence rates, such as Asia-Pacific. Collaborations between academia, private industry, and governments may also accelerate research and access to innovative therapies.

Challenges

Despite the advancements, the esophageal cancer market continues to face significant challenges. One of the most critical issues is the high mortality rate, with 5-year survival remaining under 20% in many regions due to late diagnosis and limited treatment response. In low- and middle-income countries, limited access to advanced diagnostic equipment and modern therapeutics hampers early intervention and long-term disease management. Cost is also a major barrier, as novel therapies like immunotherapy are expensive and may not be covered under public health systems or insurance plans.

Furthermore, side effects associated with chemoradiation and immunotherapies can reduce patient compliance and quality of life. Regulatory hurdles and lengthy clinical approval timelines can also slow the introduction of new treatments into the market. Lastly, the market suffers from disparities in care, with rural and economically disadvantaged populations having limited access to specialized oncology services.

Esophageal Cancer Market Companies

- F. Hoffmann-La Roche Ltd

- Merck & Co., Inc.

- Bristol-Myers Squibb Company

- Pfizer Inc.

- AstraZeneca plc

- Eli Lilly and Company

- Novartis AG

- Amgen Inc.

- Johnson & Johnson (Janssen Biotech)

- Daiichi Sankyo Company, Limited

- GlaxoSmithKline plc (GSK)

- Bayer AG

- AbbVie Inc.

- Takeda Pharmaceutical Company Limited

- Illumina, Inc. (diagnostics)

- Thermo Fisher Scientific Inc. (diagnostics)

Segments Covered in the Report

By Cancer Type

- Adenocarcinoma (Fastest)

- Squamous Cell Carcinoma (Largest – 80%)

- Others (e.g., small cell carcinoma)

By Diagnosis

- Endoscopy (Largest – 40%)

- Biopsy

- Barium Swallow (Esophagram)

- Imaging (CT, PET, MRI) (Fastest)

- Esophageal Manometry

- Blood Tests

By Treatment

- Therapy Type (Fastest and Largest 60%)

- Chemotherapy

- Radiation Therapy

- Targeted Therapy

- Immunotherapy (e.g., checkpoint inhibitors)

- Surgery

- Endoscopic Treatments (e.g., mucosal resection)

- Palliative Care

- Drug Class

- PD-1/PD-L1 Inhibitors

- HER2 Inhibitors

- VEGF Inhibitors

- Cytotoxic Agents

- Tyrosine Kinase Inhibitors (TKIs)

- Antimetabolites

- Others

By Stage

- Stage 0 (Carcinoma in situ)

- Stage I

- Stage II (Fastest and Largest – 35%)

- Stage III

- Stage IV (Metastatic)

By Route of Administration

- Oral (Notable)

- Intravenous (Fastest and Largest – 85%)

- Others

By End User

- Hospitals (Largest – 70%)

- Specialty Cancer Centers

- Academic & Research Institutes

- Ambulatory Surgical Centers (ASCs) (Fastest)

- Homecare Settings

By Distribution Channel

- Hospital Pharmacies (Largest – 60%)

- Retail Pharmacies

- Online Pharmacies (Fastest)

By Region

- North America (Largest – 40%)

- Europe

- Asia Pacific (Fastest)

- MEA

- South America

Read Also: Photochromic Materials Market

You can place an order or ask any questions, please feel free to contact at sales@precedenceresearch.com|+1 804 441 9344