by

by Table of Contents

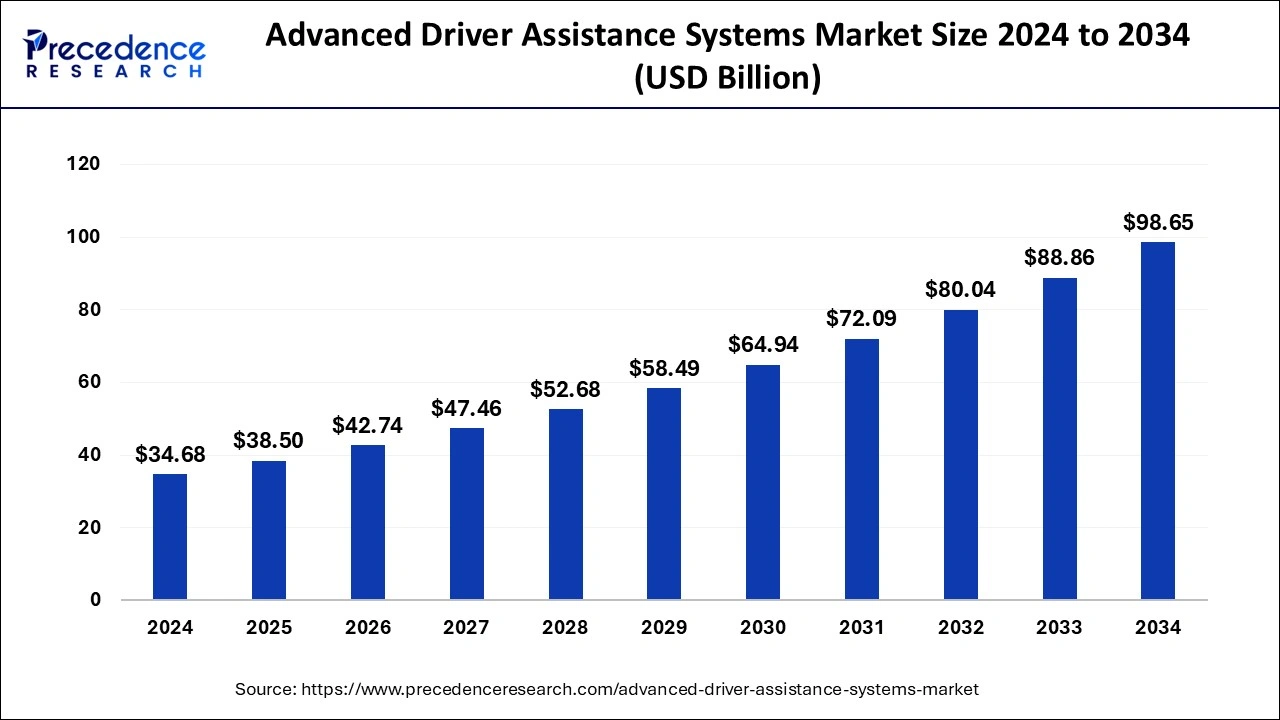

The global Advanced Driver Assistance Systems (ADAS) market is valued at USD 38.50 billion in 2025 and is projected to reach approximately USD 98.65 billion by 2034, expanding at a CAGR of 11.02% during 2025–2034.

Key Highlights of the Advanced Driver Assistance Systems Market

-

LiDAR sensors held a notable market share by component type in 2024.

-

The software segment is expected to record a strong CAGR from 2025 to 2034.

-

By vehicle category, commercial cars are forecast to grow at a CAGR of 17.3%.

-

In 2024, the tire pressure monitoring system (TPMS) segment accounted for over 20.7% of the market share by solution type.

-

Autonomous emergency braking (AEB) is anticipated to witness the fastest growth, with a CAGR of 21.5% through the forecast period.

The Role of AI in Transforming the ADAS Industry

Artificial Intelligence (AI) is fundamentally reshaping the ADAS sector by improving vehicle safety, automation, and real-time decision-making capabilities. Advanced AI algorithms analyze massive volumes of sensor data from LiDAR, radar, and cameras to enhance object recognition, lane-keeping systems, and adaptive cruise control.

Machine learning enables predictive collision avoidance and supports real-time driver assistance to reduce human error. AI also powers autonomous emergency braking and driver monitoring systems, resulting in more responsive and intelligent vehicles. As AI evolves, ADAS will advance toward fully autonomous, highly efficient driving systems.

U.S. Advanced Driver Assistance Systems Market Outlook (2025–2034)

The U.S. ADAS market, valued at USD 7.80 billion in 2024, is projected to reach around USD 22.36 billion by 2034, reflecting a CAGR of 11.10% from 2025 to 2034.

North America leads globally, driven by strict safety regulations, rapid adoption of advanced automotive technologies, and the presence of top car manufacturers.

Europe follows closely, backed by Euro NCAP safety mandates and incentives for autonomous driving tech.

Asia-Pacific is witnessing fast-paced growth due to higher vehicle production, rising income levels, and strong government support for safety features.

Country highlights:

-

China, Japan, and South Korea are spearheading innovations in AI-driven ADAS technologies.

-

In China, companies like XPeng and Huawei are developing software capable of mimicking human driving behaviors and managing complex traffic conditions, with government policies accelerating adoption.

Advanced Driver Assistance Systems Market Regional Insights

North America

Holds the largest market share, supported by rigorous safety laws, widespread technology acceptance, and a mature automotive ecosystem. Consumer demand for advanced safety features is fueling continuous adoption.

Europe

Experiences consistent growth, supported by strict safety norms and a strong manufacturing base. Germany leads regional revenue due to its high-end automobile production and strong consumer preference for ADAS-enabled models.

Asia-Pacific

Emerging as a high-growth market, with substantial investments in autonomous driving R&D. Supportive government policies and fast technology deployment are accelerating adoption rates.

Advanced Driver Assistance Systems Market Overview

| Report Coverage | Details |

|---|---|

| Market Size in 2025 | USD 38.50 Billion |

| Market Size by 2034 | USD 98.65 Billion |

| CAGR (2025–2034) | 11.02% |

| Largest Market | North America |

| Base Year | 2024 |

| Forecast Period | 2025–2034 |

| Segments Covered | System Type, Vehicle Type, Sensor Type, Electric Vehicle, Level of Autonomy, Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East & Africa |

Drivers

-

Heightened global emphasis on vehicle safety regulations.

-

Rising demand for autonomous and semi-autonomous vehicles.

-

Mandatory implementation of systems like lane departure warning, adaptive cruise control, and automatic emergency braking.

-

Increasing public awareness about road safety and accident prevention.

-

Advancements in AI, sensors, and connected vehicle technologies improving system reliability and performance.

Opportunities

-

Rapid AI and machine learning integration into ADAS.

-

Growing adoption of electric vehicles and connected cars.

-

Deployment of 5G networks enabling faster vehicle-to-vehicle and vehicle-to-infrastructure communication.

-

Expanding opportunities in emerging markets like Asia-Pacific and Latin America, supported by safety legislation and rising vehicle production.

Challenges

-

High installation costs limiting adoption in budget and mid-range vehicles.

-

Complexity in integrating ADAS with legacy automotive systems.

-

Cybersecurity and data privacy concerns in connected systems.

-

Environmental factors like poor weather and road infrastructure limitations affecting performance accuracy.

Advanced Driver Assistance Systems Market Companies

-

Denso

-

Aptiv

-

Robert Bosch GmbH

-

Continental AG

-

Magna International

-

Veoneer

-

Hyundai Mobis

-

ZF Friedrichshafen

-

Valeo

-

NVIDIA

-

Intel

-

Microsemi Corporation

-

Nidec Corporation

-

Hella

-

Texas Instruments

-

Infineon Technologies AG

-

Hitachi Automotive

-

Renesas Electronics Corporation

Advanced Driver Assistance Systems Market Segmentation

By System Type

-

Intelligent Park Assist (IPA)

-

Lane Departure Warning (LDW)

-

Road Sign Recognition (RSR)

-

Tire Pressure Monitoring System (TPMS)

-

Night Vision System (NVS)

-

Automatic Emergency Braking (AEB)

-

Adaptive Cruise Control (ACC)

-

Adaptive Front Light (AFL)

-

Blind Spot Detection (BSD)

-

Cross Traffic Alert (CTA)

-

Driver Monitoring System (DMS)

-

Forward Collision Warning (FCW)

-

Others

By Sensor Type

-

Image Sensors

-

Ultrasonic Sensors

-

LiDAR

-

Radar Sensors

-

Infrared (IR) Sensors

-

Laser Sensors

By Vehicle Type

-

Passenger Car

-

Light Commercial Vehicle

-

Truck

-

Bus

By Level of Autonomy

-

L1

-

L2

-

L3

-

L4

-

L5

By Electric Vehicle

-

Battery Electric Vehicles (BEV)

-

Hybrid Electric Vehicles (HEV)

-

Plug-in Hybrid Electric Vehicles (PHEV)

-

Fuel Cell Electric Vehicles (FCEV)

By Geography

North America

-

U.S.

-

Canada

Europe

-

U.K.

-

Germany

-

France

Asia-Pacific

-

China

-

India

-

Japan

-

South Korea

-

Malaysia

-

Philippines

Latin America

-

Brazil

-

Rest of Latin America

Middle East & Africa (MEA)

-

GCC

-

North Africa

-

South Africa

-

Rest of MEA

Read Also: Semiconductor Etch Equipment Market

You can place an order or ask any questions, please feel free to contact us at sales@precedenceresearch.com |+1 804 441 9344