by

by Table of Contents

- Asia Pacific led the market in 2024, capturing the largest revenue share of 41%, while North America is anticipated to witness considerable growth during the forecast period.

-

By type of chamber, temperature and humidity chambers dominated with a 36% market share in 2024, whereas thermal shock chambers are expected to grow at the fastest pace through 2034.

-

In terms of form factor/design, reach-in chambers held the top spot with a 34% share in 2024, while modular chambers are forecasted to exhibit the highest growth rate.

-

On the basis of application, the automotive sector accounted for the leading share of 29% in 2024, whereas the electronics & semiconductors segment is projected to expand significantly in the coming years.

-

By testing parameter, temperature testing was the dominant category with a 31% share in 2024, while combined environment testing is poised for substantial growth over the forecast period.

-

Regarding the cooling mechanism, the air-cooled segment held the largest share of 42% in 2024, with cryogenic-cooled systems expected to grow at the fastest CAGR through 2034.

-

In terms of control systems, digital/programmable controllers led the market with a 40% share in 2024, while cloud-connected (IoT-enabled) systems are projected to experience strong growth.

-

By end-user, OEMs represented the largest share of 38% in 2024, while the test laboratories segment is expected to witness the fastest growth rate during the forecast period.

Impact of AI and Smart Technologies in Environmental Test Chambers Market

Artificial intelligence and smart technologies are redefining how environmental test chambers operate. Key innovations include:

-

AI-driven predictive analytics to determine test duration and failure probability,

-

Machine learning algorithms for auto-calibration and test optimization,

-

Cloud integration for managing test data across global R&D hubs,

-

Digital twins for simulating test environments virtually before physical testing begins.

Environmental Test Chambers Market Key Growth Segments Analysis

1. Chamber Types

-

Temperature and Humidity Chambers dominate the market due to their critical role in simulating climate-based wear and stress conditions for electronic and automotive components.

-

Thermal Shock Chambers are experiencing increased adoption in the aerospace and defense sectors. These systems expose products to sudden temperature fluctuations to test their integrity under real-world extremes.

2. Form Factors

-

Reach-in Chambers continue to be widely adopted in R&D labs and quality assurance environments due to their compact design and versatility.

-

Modular and Walk-in Chambers are growing in popularity for high-volume and large-scale testing, particularly in the automotive and semiconductor industries, offering scalability and customization for multiple testing parameters.

3. Applications

-

The automotive industry leads in usage, especially for testing battery packs, EV components, and ADAS (Advanced Driver-Assistance Systems), under varying environmental conditions.

-

The electronics sector is another significant contributor, using environmental chambers to test semiconductors, printed circuit boards (PCBs), and consumer electronics for thermal and humidity resilience.

4. Testing Parameters

-

Temperature Testing remains the most essential parameter across industries, critical for evaluating operational thresholds and failure points.

-

Combined Environment Testing—integrating temperature, humidity, vibration, and altitude—is gaining traction as product use cases become more complex and multifunctional.

5. Cooling Mechanisms and Control Systems

-

Air-Cooled Systems are favored for their energy efficiency and lower maintenance in smaller form factors.

-

Cryogenic-Cooled Chambers are increasingly used in defense and aerospace for simulating extreme sub-zero conditions.

-

IoT-Enabled and Programmable Controllers are revolutionizing test management, offering real-time data capture, remote monitoring, and predictive maintenance capabilities.

Environmental Test Chambers Market Scope

| Report Coverage | Details |

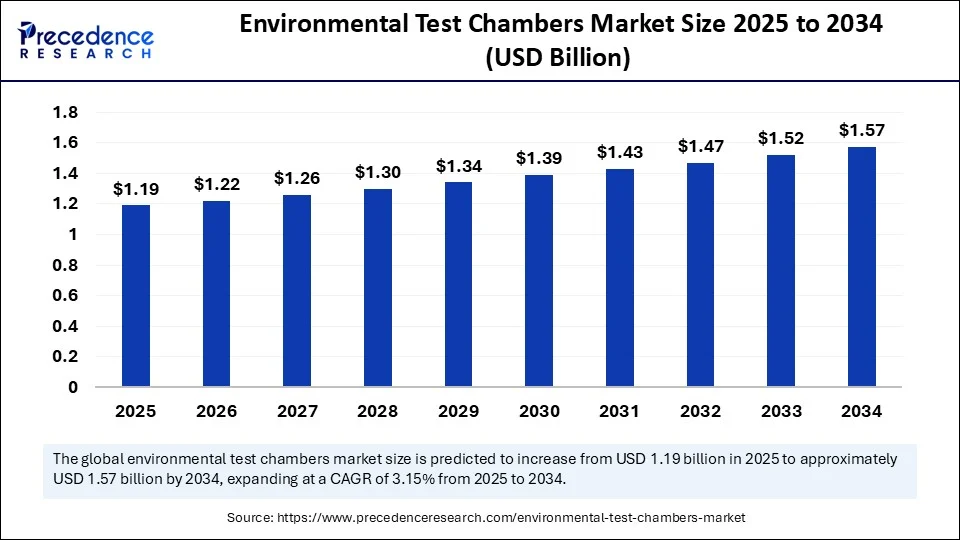

| Market Size by 2034 | USD 1.57 Billion |

| Market Size in 2025 | USD 1.19 Billion |

| Market Size in 2024 | USD 1.15 Billion |

| Market Growth Rate from 2025 to 2034 | CAGR of 3.15% |

| Dominating Region | Asia Pacific |

| Fastest Growing Region | North America |

| Base Year | 2024 |

| Forecast Period | 2025 to 2034 |

| Segments Covered | Type of Chamber, Form Factor, Application, Testing Parameter, Cooling Mechanism, Control System, End-User, and Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Environmental Test Chambers Market Regional Analysis

Asia Pacific

Asia Pacific remains the largest and fastest-growing market, accounting for over 40% of global revenue in 2024. China, in particular, plays a dominant role due to its massive electronics manufacturing base and growing automotive R&D infrastructure. Increasing domestic innovation and stricter product certification standards are further boosting demand for environmental testing solutions.

North America

The North American market is projected to experience strong growth, driven by:

-

Adoption of advanced R&D in aerospace and electric vehicles (EVs),

-

Stricter FDA and ISO standards,

-

Robust defense spending encouraging high-performance testing environments.

Europe

Europe is increasingly aligning its industrial processes with sustainability objectives. Environmental test chambers that support energy-efficient testing, recyclable refrigerants, and eco-friendly materials are gaining momentum. Germany and the UK are at the forefront, especially in automotive and renewable energy sectors.

Challenges and Opportunities

Challenges

-

Lack of technical expertise in operating and maintaining sophisticated testing systems remains a significant barrier in emerging markets.

-

Integration complexity with legacy manufacturing systems can delay adoption and increase implementation costs.

-

High customization demands from end-users necessitate modular and adaptable designs, raising production costs for manufacturers.

Opportunities

-

Rising demand for multifunctional chambers capable of performing multiple stress tests in one cycle.

-

Increasing focus on regulatory compliance and quality certification is prompting SMEs to invest in test chambers.

-

Growing emphasis on safety and reliability in emerging sectors such as electric mobility, 5G infrastructure, and IoT devices presents untapped opportunities for solution providers.

Environmental Test Chambers Market Companies

- Thermotron Industries

- Weiss Technik (Weiss Umwelttechnik GmbH)

- ESPEC Corp.

- CSZ (Cincinnati Sub-Zero)

- Tenney Environmental (TPS)

- Russells Technical Products

- Binder GmbH

- Memmert GmbH + Co.KG

- Angelantoni Test Technologies

- ETS Lindgren

- Climats

- KOMEG Technology

- Zhongzhi Testing Equipment

- Thermal Product Solutions (TPS)

- Qualmark Corporation (a HALT/HASS brand by ESPEC)

- Hastest Solutions

- Ineltec

- Associated Environmental Systems (AES)

- BINDER Environmental Testing Chambers

- FEMTO-ST

Conclusion and Future Outlook

The Environmental Test Chambers market is undergoing a transformation fueled by technological innovation, regulatory pressures, and growing industry demand for precision and reliability. Through 2034, the industry will increasingly pivot toward:

-

Smart, connected systems with AI integration,

-

Sustainability-driven designs with reduced energy consumption,

-

Highly customizable, multifunctional chambers catering to next-gen applications in EVs, 5G, and advanced electronics.

Read Also: Butter Packaging Market

You can place an order or ask any questions, please feel free to contact at sales@precedenceresearch.com |+1 804 441 9344