by

by

Ambulatory Infusion Centers Market Key Highlights

-

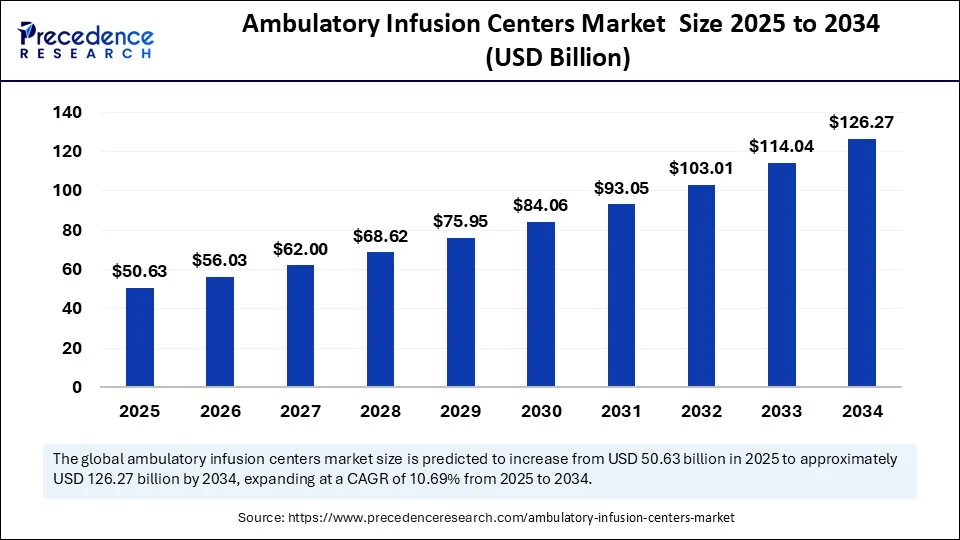

The global ambulatory infusion centers market was valued at USD 45.76 billion in 2024 and is projected to reach USD 126.27 billion by 2034, growing at a CAGR of 10.69% from 2025 to 2034.

-

North America dominated the market in 2024 with a 58% share, while the Asia Pacific region is anticipated to register the fastest CAGR during the forecast period.

-

By therapy type, biological therapy held the largest market share at 28% in 2024, while immunoglobulin therapy is expected to grow at a remarkable CAGR through 2034.

-

Based on application, the autoimmune disorders segment led the market with a 33% share in 2024, whereas the oncology segment is projected to expand at a notable CAGR in the coming years.

-

In terms of end user, standalone/independent infusion centers accounted for the largest share at 42% in 2024, while physician office infusion centers are expected to grow significantly during the forecast period.

-

By payor type, commercial insurance was the leading segment with a 48% share in 2024, and the Medicare segment is expected to grow at a notable CAGR over the projected timeline.

Ambulatory Infusion Centers Market Overview

The global ambulatory infusion centers market has experienced significant growth in recent years and is poised for continued expansion over the coming decade. Valued at approximately USD 45.76 billion in 2024, the market is projected to reach USD 126.27 billion by 2034, growing at a CAGR of 10.69% from 2025 to 2034. Ambulatory infusion centers (AICs) provide outpatient infusion therapy, allowing patients to receive intravenous (IV) medications without the need for hospitalization.

These centers serve a wide range of therapeutic areas including oncology, rheumatology, immunology, and infectious diseases. Their cost-effectiveness, convenience, and ability to reduce inpatient burden on hospitals have made them an increasingly preferred option among patients and healthcare providers alike. Furthermore, the rising prevalence of chronic diseases, along with a strong push for value-based care models globally, has significantly boosted demand for outpatient care options such as AICs.

Ambulatory Infusion Centers Market Growth Factors

Several critical factors are contributing to the growth of the ambulatory infusion centers market. First, the increasing incidence of chronic diseases such as cancer, autoimmune disorders, and neurological conditions has amplified the need for long-term and repeated infusion treatments. Second, the shift from inpatient to outpatient care—driven by the need to reduce healthcare costs—is pushing healthcare systems and payers to favor ambulatory infusion setups.

Technological advancements in infusion equipment and therapies are also enhancing treatment efficiency and patient comfort. Moreover, government initiatives in developed economies to promote cost-effective and high-quality healthcare delivery are fostering the establishment of more outpatient infusion centers.

Reimbursement improvements, particularly in the U.S., for infusion therapies provided in outpatient settings have also made these services more accessible and profitable, thus encouraging investments in the sector.

Role of AI in the Ambulatory Infusion Centers Market

Artificial intelligence (AI) is beginning to reshape the ambulatory infusion centers market by streamlining operational processes, enhancing patient care, and optimizing resource utilization. AI-driven predictive analytics tools are being used to forecast patient volumes, schedule appointments, and allocate staff and infusion chairs more efficiently. These tools help reduce wait times, avoid bottlenecks, and improve overall workflow.

In clinical applications, AI is playing a role in precision dosing, identifying adverse reactions in real-time, and personalizing infusion regimens based on patient history and response patterns. Chatbots and virtual assistants are increasingly being deployed for patient engagement, appointment reminders, and pre-infusion screenings. Furthermore, AI-assisted remote monitoring tools are allowing care teams to track patients’ vital signs and infusion responses, improving safety and outcomes. Over the coming years, AI integration is expected to further enhance the scalability and cost-effectiveness of ambulatory infusion centers.

Market Drivers

The market is primarily driven by the growing burden of chronic diseases that require recurring infusion therapies, such as cancer, multiple sclerosis, and Crohn’s disease. The rising geriatric population, which is more susceptible to such conditions, is further propelling demand. A strong preference among patients for outpatient care due to its convenience and lower costs is another key driver. Healthcare reforms favoring bundled payments and value-based care models are also pushing providers to opt for ambulatory infusion services.

Advancements in biologic drugs and specialty pharmaceuticals that require infusion-based administration have broadened the treatment portfolio offered by AICs, enhancing their market potential. The ongoing digital transformation of healthcare, including the incorporation of electronic health records (EHRs), telemedicine, and remote monitoring, is facilitating seamless coordination of care in outpatient settings, making them more appealing to both patients and providers.

Opportunities

The ambulatory infusion centers market presents significant opportunities for expansion, particularly in developing regions where healthcare infrastructure is rapidly evolving. Strategic partnerships between pharmaceutical companies and infusion center operators can lead to specialized care pathways for newly approved biologics and infusion therapies. There is also immense potential in rural and semi-urban areas where hospital access is limited, and outpatient infusion centers can bridge the gap in care delivery.

Moreover, increased investment in home-infusion-aligned ambulatory models opens a hybrid channel for expansion, catering to patients who need supervised but non-hospital-based treatment. Adoption of AI and machine learning technologies offers a competitive edge for centers that prioritize efficiency and personalized care. Furthermore, growing investor interest in outpatient service chains, as seen through private equity-backed roll-ups of infusion networks, is expected to drive industry consolidation and innovation.

Challenges

Despite the promising outlook, the ambulatory infusion centers market faces several challenges. One of the major barriers is the complexity and variability of reimbursement policies across regions and payers, which can hinder consistent revenue streams. Operational challenges, including staffing shortages of specialized nurses and pharmacists, can affect service quality and scalability.

The high cost of biologic and specialty drugs used in infusion therapies may limit affordability and access for patients in low-income settings. Regulatory compliance and maintaining high standards of infection control and drug handling are crucial and require significant investment.

Moreover, integrating advanced technologies such as AI and EHRs into existing systems can be resource-intensive and may face resistance from staff due to lack of training or fear of job displacement. These challenges necessitate strategic planning, policy support, and continuous investment in infrastructure and human capital.

Regional Outlook

Geographically, North America dominated the ambulatory infusion centers market in 2024, accounting for a 58% market share, driven by a mature healthcare system, favorable reimbursement structures, and high demand for outpatient services. The U.S. in particular has seen a proliferation of standalone infusion clinics and hospital-affiliated centers, supported by Medicare and private payer policies that incentivize outpatient care.

Europe holds a significant share, with countries like Germany, the U.K., and France leading in outpatient care innovation and public-private collaboration in healthcare delivery.

Asia Pacific is projected to witness the fastest growth rate over the forecast period, spurred by a growing middle class, urbanization, increased healthcare spending, and rising awareness of chronic disease management. Countries such as China, India, and Japan are investing in outpatient infrastructure to reduce hospital burdens and improve care accessibility.

Latin America and the Middle East & Africa present untapped opportunities, although limited by regulatory hurdles, infrastructural constraints, and affordability issues. Strategic market entry by global players and public health initiatives in these regions could unlock long-term growth potential.

Ambulatory Infusion Centers Market Companies

- Option Care Health

- InfuCare Rx

- Coram CVS (now part of Option Care)

- KabaFusion

- BioScrip (now part of Option Care)

- Amerita (a PharMerica company)

- United Infusion

- Soleo Health

- Paragon Healthcare

- PromptCare

- ContinuumRx

- CareCentrix

- Chartwell Pennsylvania

- Intramed Plus

- AlayaCare

- ClearSky Health

- Healix Infusion Therapy

- Nufactor (a FFF Enterprises company)

- PharMerica Infusion Services

- Infusion Associates

Segments Covered in the Report

By Therapy Type

- Anti-infective Therapy

- Hydration Therapy

- Chemotherapy

- Immunoglobulin Therapy

- Biological Therapy

- Enteral and Parenteral Nutrition

- Others (e.g., corticosteroids, pain management infusions)

By Application

- Oncology

- Autoimmune Disorders

- Rheumatoid Arthritis

- Multiple Sclerosis

- Crohn’s Disease

- Psoriasis

- Neurological Disorders

- Infectious Diseases

- Gastrointestinal Disorders

- Immune Deficiencies

- Others

By End-User

- Hospital-Affiliated Infusion Centers

- Physician Office Infusion Centers (POICs)

- Standalone/Independent Infusion Centers

- Home Infusion Service Providers (with ambulatory setups)

By Payor Type

- Commercial Insurance

- Medicare

- Medicaid

- Out-of-Pocket / Self-Pay

Read Also: DDoS Protection and Mitigation Market

You can place an order or ask any questions, please feel free to contact at sales@precedenceresearch.com |+1 804 441 9344